Tungsten Market Overview Analysis By Fortune Business Insights

Market Summary

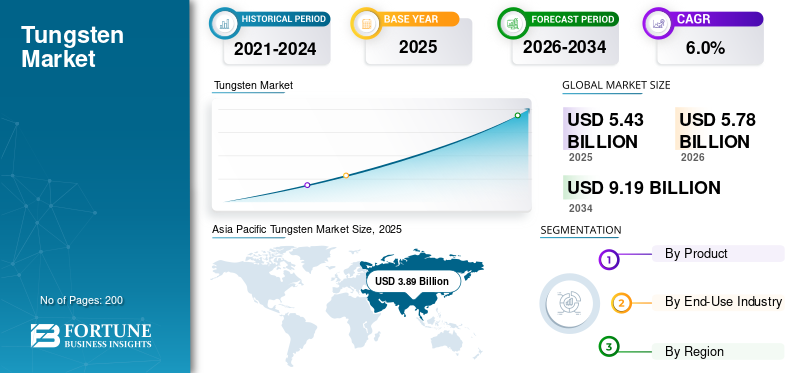

According to Fortune Business Insights: The global tungsten market size was valued at USD 5.43 billion in 2025 and is projected to grow from USD 5.78 billion in 2026 to USD 9.19 billion by 2034, exhibiting a CAGR of 6.0% during the forecast period. Tungsten is a refractory metal distinguished by the highest melting point of all known metals at approximately 3,422°C, combined with exceptional hardness, thermal stability, and corrosion resistance. These properties make it indispensable in cemented carbide tooling, high-temperature alloys, mill products, and specialty components across the mining, construction, automotive, aerospace, and defense sectors. Asia Pacific dominated the market with a 71.64% share in 2025, underpinned by China's commanding role as both the world's leading tungsten producer and its largest downstream consumer.

Get a Sample Research PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/115884

Key Market Drivers

Expanding mining activities and the rising global demand for wear-resistant tooling are the primary market drivers. Mining operations are inherently demanding environments — characterized by extreme abrasion, sustained pressure, and elevated temperatures — that require tooling materials with superior hardness and durability. Tungsten carbide is the material of choice for drilling bits, rock-crushing equipment, and cutting tools in extraction settings, as it substantially outperforms conventional tool steels in service life, operational reliability, and maintenance intervals. According to the U.S. Geological Survey, approximately 60% of tungsten consumed globally is used in cemented carbides, with mining, construction, and metalworking collectively accounting for the largest share of this consumption. As global demand for minerals, metals, and energy resources continues to rise, extraction activity is expanding across both established and emerging mining markets, driving sustained incremental demand for tungsten carbide components.

The broadening of industrial and precision manufacturing activity is a reinforcing driver. Aerospace, automotive, electronics, and industrial machinery sectors increasingly require materials that maintain performance under extreme mechanical and thermal loads. Tungsten-based alloys and carbide grades are gaining wider specification in high-precision cutting tools, wear-resistant components, and aerospace structural parts, supporting improved manufacturing efficiency and extended component life. According to the International Tungsten Industry Association (ITIA), approximately 60–65% of global tungsten consumption is directed to cemented carbides, reflecting the pervasive dependence of modern heavy industry on this material class.

Market Restraints and Challenges

The most significant structural constraint on market expansion is the high geographic concentration of tungsten supply. According to the USGS, China accounted for approximately 82% of global tungsten mine production in 2025 — a level of single-country dependence that creates material supply risks for downstream manufacturers worldwide. Export controls, trade policy adjustments, or disruptions to Chinese mining and processing output can trigger rapid price volatility and supply shortages for industries operating on tight tooling inventories. Developing alternative supply sources requires substantial capital investment, long project timelines, and rigorous environmental permitting, limiting the pace at which supply diversification can realistically occur.

Recycling complexity and processing costs present additional challenges. Tungsten carbide and high-performance alloys are exceptionally hard and chemically stable — properties that make them technically demanding and costly to recycle. Recovery of usable tungsten from scrap requires specialized high-temperature processing and advanced metallurgical techniques, raising the effective cost of secondary production relative to many other industrial metals and constraining the circular economy contribution of recycled material to the overall supply balance.

Segmentation Analysis

By product, the carbide segment holds the largest market share by a substantial margin. Tungsten carbide is the foundational material for cutting, drilling, and wear-resistant applications across virtually all major end-use industries. Its combination of hardness second only to diamond, high-temperature stability, and abrasion resistance enables carbide tools to maintain performance in the most demanding operating environments — from deep-hole drilling in underground mining to high-speed machining of aerospace alloys. Kennametal notes that conventional tungsten carbide powders are used in hard metal-cutting tools, mining and road construction tools, dies, and wear parts — illustrating the breadth of carbide's industrial penetration. The mill products segment, comprising sheet, rods, and plates, is expected to grow at a CAGR of 5.4% through 2034, driven by expanding demand for tungsten-based stock material in precision engineering, defense, and specialty electronics applications. The alloys segment serves aerospace, defense, and radiation shielding end uses requiring high-density, high-strength structural materials.

By end-use industry, mining leads market demand, reflecting tungsten carbide's central role in extraction tooling and wear components for heavy drilling, excavation, and rock-crushing equipment. The construction segment is expected to grow at the fastest CAGR of 6.2%, driven by accelerating global infrastructure investment and the broadening use of tungsten carbide in concrete cutting tools, road milling equipment, and earthmoving machinery. Automotive demand is sustained by tungsten's use in precision machining tools for engine components, transmission parts, and lightweight structural assemblies. Aerospace and defense applications leverage tungsten's high density, thermal resistance, and structural strength in turbine blades, radiation shielding, kinetic energy penetrators, and aircraft structural components.

Regional Outlook

Asia Pacific is the dominant regional market, valued at USD 3.89 billion in 2025 and expected to reach USD 4.15 billion in 2026. China alone accounted for USD 2.93 billion in 2025 — approximately 75.3% of regional revenues — supported by extensive domestic tungsten ore reserves, a large vertically integrated carbide and tool manufacturing sector, and strong end-use demand from mining, construction, automotive, and machinery industries. Japan and South Korea contribute high-value downstream demand in precision tooling and advanced manufacturing. Europe maintained a valuation of USD 0.82 billion in 2025, with Germany (USD 0.20 billion) leading regional consumption through its automotive, machinery, metalworking, and industrial equipment sectors. North America reached USD 0.50 billion in 2025, with the U.S. (USD 0.44 billion) driving demand through metalworking, aerospace, defense-related applications, and a growing national focus on securing critical mineral supply chains. Latin America reached USD 0.16 billion, with Brazil (USD 0.08 billion) supported by strong mining and infrastructure development. The Middle East and Africa contributed USD 0.05 billion, with gradual growth expected as mining activity and industrial development expand.

Connect with Our Expert for any Queries: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/115884

Competitive Landscape

The global tungsten market is moderately consolidated, with barriers shaped by the capital intensity of mining and refining operations, technical demands of powder metallurgy, and the need for consistent quality across a broad product range. Key players profiled include Masan High-Tech Materials Corporation (Vietnam), H.C. Starck Tungsten GmbH (Germany), Global Tungsten & Powders (U.S.), Wolfram Bergbau und Hütten AG (Austria), Kennametal Inc. (U.S.), Sumitomo Electric Industries (Japan), Japan New Metals Co. (Japan), Umicore (Belgium), Buffalo Tungsten Inc. (U.S.), and Elmet Technologies (U.S.). In September 2024, Elmet Technologies entered a long-term offtake agreement with EQ Resources to strengthen tungsten concentrate supply for downstream manufacturing, illustrating the strategic priority major players place on securing upstream raw material access amid global supply concentration concerns.