Solid Waste Management Market Overview Analysis By Fortune Business Insights

Market Summary

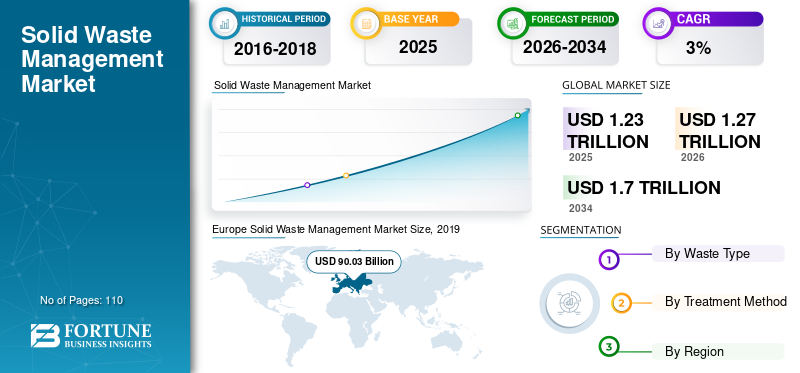

According to Fortune Business Insights: The global solid waste management market size was valued at USD 1.23 trillion in 2025 and is projected to grow from USD 1.27 trillion in 2026 to USD 1.70 trillion by 2034, at a CAGR of 3.70% during the forecast period. Solid waste encompasses unwanted solid material generated from residential, commercial, and industrial operations — primarily organic matter, paper, plastic, glass, and metal products. Solid waste management refers to the systematic collection, processing, and disposal of this material to safeguard public health and protect the environment. Europe led the global market with a 31.57% share in 2025, valued at USD 90.03 billion, while Asia Pacific is expected to register the fastest regional growth over the forecast horizon.

Get a Sample Research PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/103045

Key Market Drivers

Rising public awareness of the health and environmental consequences of improper waste handling is the primary force driving market growth. Greater access to information has elevated understanding of how hazardous solid waste affects air, water, and soil quality, as well as the spread of vector-borne diseases. Waste management campaigns by organizations such as the International Solid Waste Association are extending this awareness into developing economies across Asia and Africa, creating new demand in previously underserved markets. Proper waste management also delivers measurable social and economic benefits, including conservation of raw materials, reduced greenhouse gas emissions — particularly methane and carbon monoxide — and improved urban aesthetics, all of which are reinforcing government commitment to the sector.

Stringent government regulations are a parallel driver. Authorities across both developed and developing economies are tightening disposal requirements for industrial waste, mandating the adoption of formal waste management systems. Circular economy policies and material recycling targets are further raising demand for professional processing and disposal services, pushing manufacturers and municipalities to upgrade legacy infrastructure.

The emergence of smart waste management technologies is an important secondary trend reshaping the market. IoT-based solutions enable real-time monitoring of bin fill levels, optimization of collection routes, automated driver scheduling, and reduction of operational costs. As sensor prices decline, smart collection systems are becoming commercially viable for a wider range of municipalities, accelerating technology adoption across both urban and peri-urban areas.

Market Restraints and Challenges

High capital and operating costs represent the most significant barrier to market expansion. Waste collection is labor-intensive, requires costly vehicle fleets, bins, and processing equipment, and demands a trained workforce capable of operating safely across diverse locations. Recruiting and retaining motivated field staff is a persistent challenge, particularly in lower-income markets where competitive wages are difficult to sustain. The need for careful handling to prevent contamination of land and water resources adds further cost and complexity to operations, constraining profitability and limiting the pace at which smaller service providers can scale.

Segmentation Analysis

By waste type, industrial waste dominated in 2025 and is expected to remain the largest and fastest-growing segment throughout the forecast period. Industries are the world's largest producers of solid waste, and rapid industrialization across developing economies — combined with strict government-imposed disposal regulations — continues to drive demand for professional waste management services. The growing importance of material recycling and circular economy frameworks reinforces this demand. The municipal waste segment is underpinned by accelerating global urbanization: the United Nations projects that the proportion of the global population residing in urban areas will rise from 55% to 68% by 2050, expanding the volume of organic matter, paper, plastic, glass, and metal requiring formal management.

By treatment method, the collection segment held the largest market share in 2026 at 56.6%, reflecting its labor-intensive nature and essential role as the entry point of the waste management chain. The disposal segment ranked second, with landfilling and open dump remaining the most widely used disposal methods for both industrial and municipal solid waste. Modern landfill operations are designed and managed to stringent safety standards and offer the secondary benefit of land reclamation for recreational and community use. Within the processing segment, recycling commanded the larger share, driven by its role in circular economy strategies, reduction of raw material consumption, and cost savings for downstream industries. Composting serves as a complementary processing route, particularly for organic fractions of municipal waste.

Regional Outlook

Europe commands the leading global market share, supported by high waste collection rates, advanced treatment infrastructure, comprehensive EU waste directives targeting landfill diversion and greenhouse gas reduction, and more than 500 operational waste-to-energy plants across the region. North America holds the second-largest share, anchored by the United States, which operates at a waste collection rate of over 98% and hosts large integrated waste management companies including Waste Management Inc., Republic Services, Covanta Holdings, and Clean Harbors. The U.S. solid waste management market is forecast to reach USD 93.46 billion by 2034. Asia Pacific is the fastest-growing region at a projected CAGR of 4.2%, propelled by rapid industrialization, population growth, and government waste treatment regulations in China and India — which together represent over 37% of the world population. Developed Asia Pacific markets including Japan, South Korea, and Australia exhibit high penetration of modern waste treatment facilities and strict environmental controls. Latin America and the Middle East and Africa are expanding steadily on the back of urban growth, public health initiatives, and improving waste collection infrastructure.

Connect with Our Expert for any Queries: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/103045

Competitive Landscape

The global solid waste management market features a mix of large multinational operators and regional specialists. Key players include Waste Management Inc. and Republic Services Inc. (U.S.), SUEZ Group and Veolia Environment (France), Biffa PLC (U.K.), Clean Harbors Inc. and Covanta Holdings Corporation (U.S.), Hitachi Zosen Corporation (Japan), Remondis AG & Co. KG and ALBA Group (Germany), Stericycle Inc., Advanced Disposal Services, and Recology (U.S.), as well as TANA Oy (Finland) and Envac Group (Sweden). Leading players are pursuing geographic expansion through mergers and acquisitions, investing in new processing facilities, and entering long-term municipal service contracts. Smart and sustainable waste management solutions and social media–driven public awareness campaigns are increasingly central to competitive strategy.