Polyvinyl Alcohol Market Overview Analysis By Fortune Business Insights

Market Summary

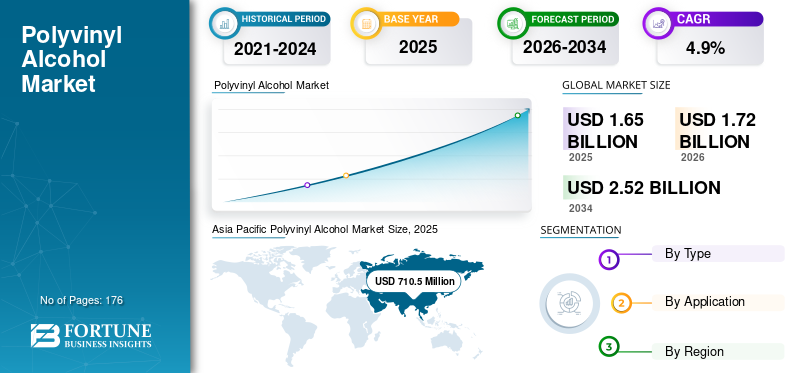

According to Fortune Business Insights: The global polyvinyl alcohol (PVA) market size is advancing at a steady pace, valued at USD 1,656.4 million in 2025 and projected to grow from USD 1,720.5 million in 2026 to USD 2,525.8 million by 2034, at a CAGR of 4.9% over the forecast period. PVA is a specialty synthetic polymer distinguished by its strong bonding performance, film-forming capability, water solubility, and resistance to oils and chemicals. It serves a diverse range of industrial applications including adhesives, paper coatings, packaging films, textiles, and construction materials. Market expansion is primarily driven by performance-based applications, growing sustainability awareness, and the gradual broadening of end-use industries, rather than any sharp spike in overall consumption volume.

Get a Sample Research PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/115908

Market Trends

A defining trend reshaping the PVA market is the rising demand for specialty grades and functional film applications that require more controlled performance characteristics. Manufacturers are developing products with tailored solubility profiles, enhanced film strength, improved barrier properties, and suitability for technical applications. This shift signals a gradual transition from standard commodity use toward higher-value, application-specific demand. Product differentiation and performance improvement are increasingly central to competitive positioning, as customers across packaging, paper, and industrial sectors demand materials that meet more exacting specifications.

Market Drivers

The primary growth driver is PVA's expanding role in packaging and paper applications, where its film-forming ability, surface strengthening, and barrier performance provide measurable processing advantages. In specialty packaging, PVA is used in soluble packaging formats and high-strength films requiring controlled dissolution. In paper manufacturing, it enhances coating performance, printability, and surface quality, making it a valued additive in high-grade paper processing. The steady rise in packaging quality requirements and the growing emphasis on functional paper coatings are sustaining robust demand across these segments.

Market Restraints

A significant constraint on market growth is PVA's heavy dependence on cyclical downstream industries such as packaging, textiles, construction, paper, and adhesives. When manufacturing activity decelerates or construction output contracts, demand from these sectors softens in tandem. Since PVA is consumed mainly in industrial and performance-driven applications, its consumption closely mirrors production trends across downstream markets. This correlation makes the market sensitive to economic slowdowns and shifting demand patterns, as reflected in a 1.4% decline in U.S. construction activity in 2025 compared to the prior year.

Market Opportunities

Water-soluble and specialty packaging applications represent a compelling growth avenue for PVA. Its unique combination of controlled dissolution, film strength, and environmental compatibility positions it well for packaging unit-dose products such as detergents and agrochemicals. As manufacturers prioritize functional and more sustainable packaging solutions, PVA's role can expand meaningfully beyond its traditional industrial base. Long-term growth is further supported by the continued innovation in specialty grades and the broadening scope of performance-driven applications across global packaging and coating sectors.

Segmentation Analysis

By Grade: Fully hydrolyzed PVA held the largest market share in 2025, driven by its high tensile strength, superior film-forming performance, and strong chemical resistance — properties essential in applications demanding durability and structural stability. Partially hydrolyzed PVA is projected to grow at a faster rate of 5.4% CAGR through 2034, supported by its solubility advantages in adhesive and coating applications. Modified and specialty grades are gaining traction as manufacturers develop formulations tailored to niche technical requirements.

By End-Use Industry: Paper remains the largest consuming segment, with PVA widely used in coating, binding, and surface treatment processes that enhance printability, pigment adhesion, and paper strength. Packaging is the fastest-growing segment, projected to expand at a 5.7% CAGR through 2034, driven by rising demand for specialty films, soluble packaging, and functional barrier materials. Other contributing segments include textiles, construction, and adhesives, where PVA's bonding and film properties deliver consistent performance value.

Regional Outlook

Asia Pacific dominated the market in 2025 with a 42.89% share, valued at USD 710.5 million, underpinned by its vast manufacturing base in paper, textiles, packaging, and industrial processing. China accounted for approximately 43.4% of regional revenues at USD 308.7 million, reflecting its deep chemical processing infrastructure and broad downstream demand. India is emerging as a growth contributor, with its market valued at USD 73.2 million in 2025, supported by expanding paper, textile, and adhesive sectors.

North America reached USD 366.7 million in 2025, driven by mature industrial demand across paper, adhesives, food packaging, and construction applications, with the U.S. alone representing USD 327.2 million — approximately 89.2% of the regional total. Europe recorded USD 392.5 million, shaped by strict environmental standards, robust paper and packaging industries, and steady demand in adhesive and construction applications. Germany and the U.K. held the largest country shares within the region. Latin America reached USD 109.0 million and the Middle East & Africa USD 77.7 million, with both regions benefiting from expanding industrial manufacturing and growing downstream processing activity.

Connect with Our Expert for any Queries: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/115908

Competitive Landscape

The PVA market is moderately consolidated, with high technical entry barriers — including complex production know-how, strict quality consistency requirements, and application-specific performance standards — limiting new participation. Leading companies such as KURARAY CO., LTD., Sekisui Specialty Chemicals America, Mitsubishi Chemical Corporation, China Petrochemical Corporation, and Denka Company Limited focus on improving product quality, expanding specialty grade portfolios, and deepening customer-specific supply relationships rather than pursuing aggressive capacity additions. Strategic priorities across key players are centered on performance enhancement, application diversification, and incremental movement into higher-value product segments to strengthen long-term market positioning.