Net Zero Energy Buildings Market Overview Analysis By Fortune Business Insights

Market Summary

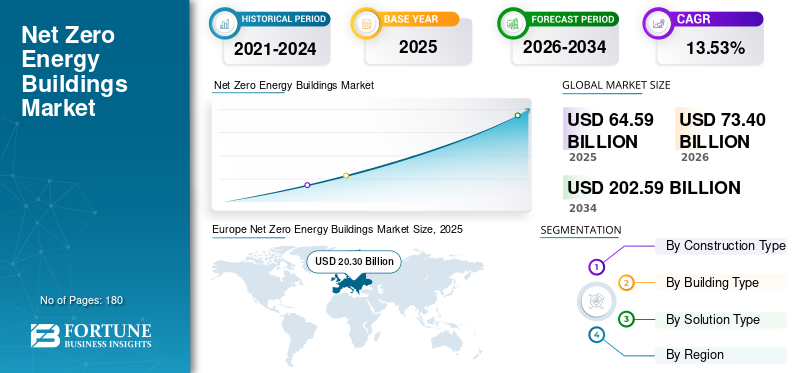

According to Fortune Business Insights: The global net zero energy buildings (NZEB) market size was valued at USD 64.59 billion in 2025 and is projected to grow from USD 73.40 billion in 2026 to USD 202.59 billion by 2034, exhibiting a CAGR of 13.53% during the forecast period. Net zero energy buildings are highly efficient structures designed to produce as much energy on-site as they consume annually across heating, cooling, lighting, and appliances. They leverage passive design principles, advanced building envelopes, and renewable energy integration to minimize demand and balance residual needs with on-site generation. The market is propelled by climate change targets, tightening regulatory frameworks, and rising occupant and investor demand for sustainable, low-cost-to-operate built environments. Europe dominated the market in 2025, supported by stringent EU energy-efficiency directives and ambitious decarbonization programs, while Asia Pacific held the second-largest share and is positioned for the fastest growth over the forecast horizon.

Get a Sample Research PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/116071

Key Market Drivers

Stringent government regulations and national net-zero targets are the primary forces driving NZEB market growth. Governments worldwide are implementing mandatory building energy codes that require near-zero or net-zero performance for new constructions and major renovations. The EU Green Deal, the revised Energy Performance of Buildings Directive, U.S. federal and state-level decarbonization policies, and national net-zero commitments are compelling developers, building owners, and institutional investors to upgrade construction and retrofit practices. Regulatory enforcement is intensifying, with penalties for non-compliance and incentives for early adoption reinforcing policy-driven demand. In November 2025, the European Commission allocated USD 3.3 billion from EU Emissions Trading System revenues to 61 net-zero technology projects across 19 sectors and 18 countries, targeting a reduction of 221 million tons of CO2-equivalent in the first decade of operation.

The acceleration of deep energy retrofit programs is a major market trend reshaping demand structure. As over 70–80% of the global building stock expected to remain in use by 2050 consists of existing structures, governments and financial institutions are prioritizing deep retrofits as a decarbonization strategy. Incentive schemes, tax rebates, mandatory renovation timelines, and green financing instruments are encouraging owners to upgrade insulation, HVAC systems, and energy controls to net-zero standards. In March 2025, the Government of Canada invested USD 10 million through the Greener Neighbourhoods Pilot for deep energy retrofits of 123 affordable townhouses in Hamilton, Ontario, delivering projected energy use reductions of 61% and emissions reductions of 90%. This shift is transforming the NZEB market from predominantly new-construction-driven to retrofit-led, broadening the addressable market significantly.

Market Restraints and Challenges

The high upfront cost of NZEB technologies remains the most significant restraint on market adoption. High-performance insulation, efficient HVAC systems, on-site renewable energy installations, battery storage, and smart building automation substantially increase initial project costs relative to conventional construction. While long-term operational savings and reduced energy bills provide a compelling financial case, the elevated capital requirements deter developers and property owners in cost-sensitive markets, and financing challenges further limit uptake among smaller-scale projects. Complex design and integration requirements add a further challenge: achieving net-zero performance demands highly coordinated, multi-disciplinary project delivery combining architectural, engineering, and energy systems expertise, increasing project timelines and risks compared to conventional development.

Segmentation Analysis

By construction type, the retrofit/renovation segment dominated in 2025 with a 55.19% share, driven by its cost-effectiveness relative to full new builds and its ability to deploy proven energy-efficient technologies — advanced insulation, solar integration, smart HVAC — into existing structures while minimizing operational disruption. New construction is the fastest-growing segment at a CAGR of 13.84%, fueled by rising demand for purpose-designed sustainable buildings, increasingly stringent building codes mandating net-zero performance from inception, and innovation in materials and integrated design approaches.

By building type, residential buildings led the market in 2025 with a 48.94% share, underpinned by growing homeowner awareness of long-term energy cost savings, government incentives for green homes, and commercially accessible advances in rooftop solar, heat pumps, and passive solar design. Commercial buildings represent the fastest-growing segment at a CAGR of 15.16%, propelled by corporate sustainability commitments, ESG-linked investment criteria, and innovations including net-zero offices with integrated microgrids, high-performance curtain wall systems, and energy-efficient building management platforms.

By solution type, energy systems held the leading share of 38.57% in 2025, reflecting the central role of high-efficiency HVAC, advanced lighting, and building automation systems in achieving on-site energy optimization. Renewable integration and smart technologies represent the fastest-growing solution segment with a CAGR of 28.14%, driven by AI-driven energy management platforms, IoT sensors, solar-plus-battery storage hybrids, and advanced grid-interactive controls that enable real-time optimization and energy independence.

Regional Outlook

Europe led the global market with USD 20.30 billion in 2025, anchored by mandatory nearly-zero energy standards across EU member states, comprehensive renovation directives, geothermal and solar integration programs, and federal green retrofit incentive funding. Germany, with a 2025 market valuation of USD 4.81 billion, and the Nordic countries lead regional adoption through passive house designs, smart building systems, and ambitious emissions-free urban development targets. Asia Pacific ranked second at USD 20.30 billion in 2025, projected to reach USD 23.91 billion in 2026, with China (USD 7.72 billion in 2025) driving adoption through aggressive government mandates and large construction pipelines, India (USD 3.15 billion) expanding through rapid urbanization and rooftop solar programs, and Japan (USD 2.97 billion) emphasizing high-quality standards and eco-friendly innovations. North America contributed USD 18.46 billion in 2025, with the U.S. market at USD 15.43 billion — representing 23.88% of global revenues — supported by federal incentives, California's zero-energy building codes, widespread solar adoption, and corporate sustainability-driven retrofit investment. Latin America is projected to reach USD 3.38 billion in 2026, led by Brazil and Mexico's green building initiatives and solar integration programs. The Middle East and Africa held a 3.19% share in 2025 at USD 2.06 billion, with GCC markets (USD 1.15 billion) advancing through UAE and Saudi Vision net-zero initiatives and dominant solar energy endowments.

Connect with Our Expert for any Queries: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/116071

Competitive Landscape

The global NZEB market is moderately consolidated, combining large multinational building technology leaders with regional specialists. Key players profiled include Siemens AG (Germany), Johnson Controls International (Ireland), Schneider Electric SE (France), Honeywell International (U.S.), ABB Ltd. (Switzerland), Daikin Industries (Japan), Carrier Global Corporation (U.S.), Trane Technologies (Ireland), Saint-Gobain (France), Kingspan Group (Ireland), Rockwool International (Denmark), Bosch Thermotechnology (Germany), Mitsubishi Electric (Japan), Panasonic (Japan), and Lennox International (U.S.). Siemens leads through its Building X AI-driven platform and a corporate pledge to achieve net-zero operations by 2030. In March 2024, Mahindra Group and Johnson Controls jointly launched the Net Zero Buildings Initiative in India, providing a free toolkit on best practices, energy assessments, and regulatory guidance to accelerate decarbonization of commercial, residential, and public buildings.