Human Fibrinogen Concentrates Market Overview Analysis By Fortune Business Insights

Market Summary

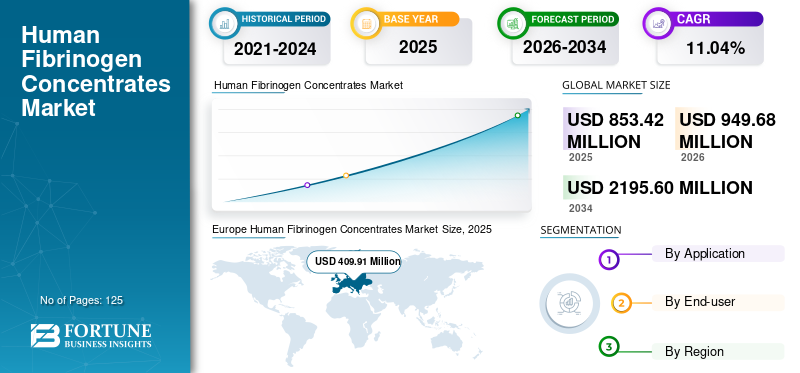

According to Fortune Business Insights: The global human fibrinogen concentrates market was valued at USD 853.4 million in 2025 and is projected to grow from USD 949.68 million in 2026 to USD 2,195.60 million by 2034, registering a compound annual growth rate (CAGR) of 11.04% over the forecast period.

Human fibrinogen concentrates are plasma-derived products designed to rapidly restore fibrinogen levels in patients experiencing serious bleeding — particularly during surgical procedures, trauma events, or in those suffering from bleeding disorders such as afibrinogenemia or hypofibrinogenemia. When fibrinogen levels fall below adequate thresholds, blood clotting time increases significantly, making external supplementation critical to patient outcomes.

Get a Sample Research PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/113876

Key Market Drivers

Rising Surgical Volume The growing burden of chronic diseases and trauma cases has led to a significant rise in surgical procedures across cardiovascular, orthopedic, neurological, and gynecological disciplines. An aging global population, higher rates of physical inactivity, and increased prevalence of lifestyle-related disorders continue to fuel surgical demand. This directly elevates the need for effective hemostatic agents, including fibrinogen concentrates.

Technological Advancements in Plasma Fractionation Innovations in plasma fractionation technology have enhanced the safety, purity, and efficacy of fibrinogen products. These improvements, combined with growing clinical awareness of advanced hemostatic therapies, are accelerating product adoption over traditional alternatives like cryoprecipitate and fresh-frozen plasma.

Shift Away from Traditional Blood Products Clinicians are increasingly favoring fibrinogen concentrates over conventional blood products due to their standardized dosing, faster administration, and elimination of the thawing process. Pipeline products such as Grifols' BT524 — which demonstrated non-inferiority to standard treatments in a Phase 3 trial — exemplify this shift toward more precise, patient-specific hemostatic solutions.

Market Restraints & Challenges

High Product Costs The complex manufacturing requirements, stringent safety protocols, and regulatory approval processes make fibrinogen concentrates expensive. For example, FIBRINOREL 1g Dried Fibrinogen is commercially priced at approximately USD 185.40 per unit. This limits accessibility in lower-income regions and restrains adoption in price-sensitive healthcare markets.

Supply Chain Complexity Manufacturing human fibrinogen concentrates requires extensive donor networks, large-scale plasma collection facilities, strict quality testing, and cold chain logistics — all of which create significant barriers to market entry. The need for highly skilled personnel for regulatory compliance and batch management adds further complexity.

Limited Reimbursement Coverage In many emerging economies, reimbursement policies for fibrinogen products remain underdeveloped, which hampers broader market penetration and slows the uptake of these advanced therapies.

Segmentation Analysis

By Application The acquired fibrinogen deficiency and surgical procedures segment is expected to hold the dominant share at approximately 92.61% in 2026, driven by the high volume of surgeries requiring hemostatic intervention. The congenital fibrinogen deficiency segment, though smaller, is expected to grow at a moderate pace, supported by increased R&D investment and funding for rare bleeding disorder treatment.

By End-User Hospitals are projected to account for approximately 83.34% of the market in 2026, reflecting their large surgical caseloads and advanced medical infrastructure. Specialty clinics represent the second-largest segment, bolstered by the expansion of specialized healthcare facilities in developing nations.

Regional Outlook

Europe leads the global market, contributing 48.03% of global revenue in 2025 at USD 409.91 million. The region benefits from the presence of major market players, well-established regulatory frameworks, and a rising prevalence of inherited blood disorders.

North America accounted for USD 204.51 million (23.96% share) in 2025, underpinned by strong healthcare infrastructure and a significant patient population with hemophilia and related disorders.

Asia Pacific held a comparable share of USD 202.63 million (23.74%) in 2025, with growth expected from an aging population, rising chronic disease burden, and expanding government and private insurance coverage for surgical procedures. Key contributors include China, Japan, and India.

Latin America and Middle East & Africa represent smaller but emerging markets, with combined revenues of approximately USD 36.36 million in 2025. Growing awareness of bleeding disorder management and increasing healthcare expenditures are expected to support growth through 2034.

Connect with Our Expert for any Queries: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/113876

Competitive Landscape

The market is moderately consolidated, with Octapharma AG, CSL (Australia), and LFB (France) holding leading positions. Other notable players include Grifols S.A. (Spain), Shanghai RAAS Blood Products Co., Ltd. (China), and Reliance Life Sciences (India).

Strategic activities are central to competitive positioning. Notable recent developments include:

- July 2025: Octapharma AG backed a USD 29 million clinical trial at the University of Colorado to study early fibrinogen replacement in trauma patients.

- June 2025: Grifols reported positive Phase 3 results for BT524 in managing acquired fibrinogen deficiency during major surgery.

- October 2024: LFB launched a new manufacturing facility to triple its bioproduction capacity for fibrinogen, albumin, and immunoglobulin.

- June 2024: Plasmagen Biosciences collaborated with CSL Behring to manufacture and commercialize Haemocomplettan P in India.

Outlook

The human fibrinogen concentrates market is positioned for robust growth through 2034, driven by the convergence of increasing surgical volumes, advancing plasma technology, strategic industry partnerships, and a global push toward more precise, evidence-based hemostatic therapies. As pipeline products mature and market access improves in developing regions, the sector presents compelling opportunities for both established players and emerging entrants.