Gift Card Market Overview Analysis By Fortune Business Insights

Market Summary

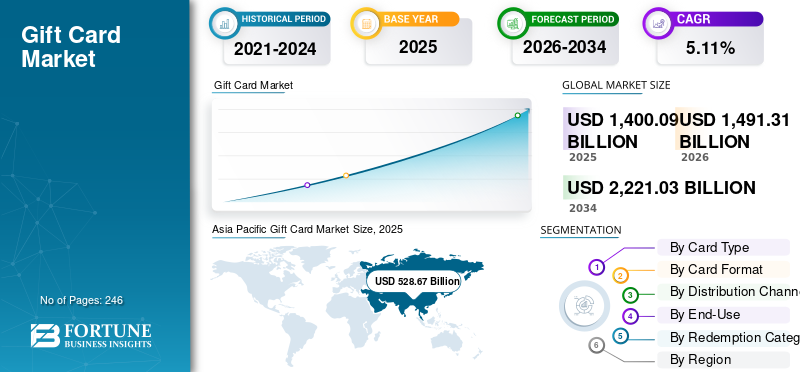

According to Fortune Business Insights: The global gift card market size is on a robust upward trajectory, valued at USD 1,400.09 billion in 2025 and projected to grow from USD 1,491.31 billion in 2026 to USD 2,221.03 billion by 2034, reflecting a compound annual growth rate (CAGR) of 5.11% over the forecast period. Gift cards — stored-value instruments redeemable for goods or services — have evolved well beyond traditional gifting into versatile tools for consumer loyalty, employee rewards, and government welfare programs. Rising internet penetration, increasing adoption of digital payment systems, and the growing appeal of gifting cards among younger, digitally native consumers are collectively fueling this market's expansion.

Get a Sample Research PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/111784

Market Drivers

A primary driver of the gift card market is retailers' consistent integration of loyalty points and cashback programs with gifting cards. By embedding rewards into the card experience, merchants strengthen customer retention while keeping spending within their ecosystems. Advances in digital payment infrastructure — including QR code-enabled cards, mobile wallet integration, and fintech portal connectivity — further enhance the usability of gift cards, encouraging wider adoption. The growing corporate sector also plays a pivotal role, as businesses increasingly rely on gift cards for employee incentive schemes, seasonal bonuses, and wellness programs, sustaining steady institutional demand.

Market Restraints

Despite its strong growth profile, the market faces notable challenges. Fraud and security vulnerabilities — encompassing money laundering, card cloning, and credential theft — erode consumer confidence and impose additional operational costs on retailers managing fraudulent code-encrypted physical cards. Regulatory complexity presents another barrier: many jurisdictions impose restrictions on expiry dates and inactivity fees, while ongoing or inconsistent policy changes make compliance difficult for companies operating across multiple international markets.

Market Segmentation

By Card Type: Closed-loop cards — restricted to specific merchants or brands — held a dominant 62.34% market share in 2025. Their popularity stems from brands' ability to retain revenue within their own networks. Open-loop cards, offering broader usability and financial ecosystem compatibility, are growing fastest at a CAGR of 5.68%.

By Card Format: Physical cards led the market in 2025 with a 54.23% share, driven by in-store gifting demand and bulk corporate distribution programs. The digital segment is gaining ground rapidly, supported by rising smartphone adoption and consumer preference for instant, contactless transactions.

By Distribution Channel: Online channels commanded a leading 61.22% share in 2025 and are projected to grow at 5.58% CAGR through 2034, as retailers leverage e-commerce platforms, digital marketplaces, and fintech portals. Offline/in-store channels remain relevant, supported by impulse purchases and promotional activities at retail outlets and shopping malls.

By End-Use: Consumer gifting is the largest segment, accounting for 60.84% of the market in 2025, driven by growing gift-giving cultures and festival celebrations. Corporate rewards and incentives represent the second major segment, with firms increasingly automating and digitizing their recognition programs.

By Redemption Category: The retail segment dominated with a 54.33% market share in 2025, underpinned by Amazon, Walmart, and other major retailers embedding gift cards in their customer acquisition strategies. The entertainment and gaming segment is expected to grow at the fastest rate of 6.69% CAGR, propelled by the rapid expansion of online gaming platforms, subscription content services, and digital incentives from platforms such as PlayStation Network and Xbox Live.

Regional Outlook

Asia Pacific led the global market with a 37.76% share in 2025, driven by mobile-first payment ecosystems, rising smartphone adoption, and robust demand for digital and gaming cards across China, India, and Southeast Asia. North America held the second-largest share, benefiting from a mature digital payments infrastructure and high seasonal gifting activity around events such as Christmas and Black Friday. Europe ranked third, with its market reaching USD 265.46 billion in 2025, supported by established corporate gifting practices and advanced online payment adoption. The Middle East and Africa region is forecast to register the fastest growth at a CAGR of 6.54%, energized by government-backed cashless payment initiatives and expanding corporate sectors in the UAE and Saudi Arabia. South America is also growing steadily, with Brazil generating USD 75.37 billion in 2025.

Connect with Our Expert for any Queries: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/111784

Competitive Landscape

The global gift card market is shaped by a concentrated group of established players including Amazon.com, Inc., Blackhawk Network Holdings, Inc. (BHN), Apple Inc., InComm Payments, and Mastercard Inc. These companies compete by expanding retailer distribution networks, forging partnerships with banks and fintech firms, and innovating in digital redemption and mobile wallet integration. Notable recent developments include VoucherCart's integration with Lightspeed Restaurant POS for digital and physical card management (December 2025), Fold's partnership with Blackhawk Network to distribute a Bitcoin gift card (August 2025), and InComm Payments' acquisition of Australia's Card Network to bolster its Asia-Pacific presence.