Computational Biology Market Overview Analysis By Fortune Business Insights

Market Summary

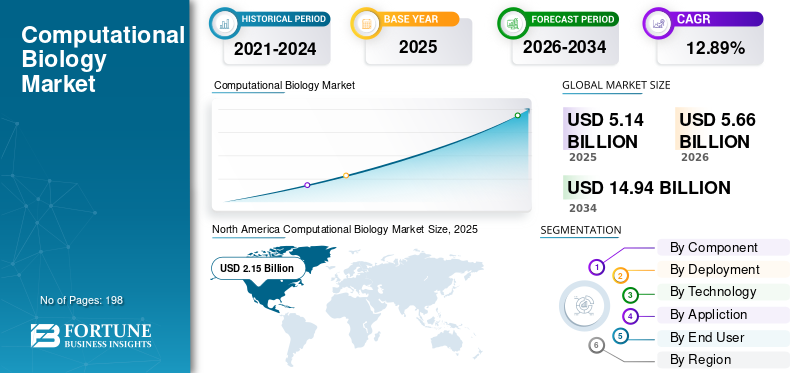

According to Fortune Business Insights: The global computational biology market size was valued at USD 5.14 billion in 2025 and is projected to grow from USD 5.66 billion in 2026 to USD 14.94 billion by 2034, at a CAGR of 12.89% during the forecast period. Computational biology encompasses methods and platforms applied to examine biological information, simulate molecular and cellular systems, and support decision-making in genomics, proteomics, drug development, biomarker discovery, and translational research. The market is driven by surging multi-omics and genomic data volumes, wider adoption of cloud-based and AI-driven research platforms, and intensifying demand for computational tools that expedite target discovery, molecular modeling, and precision medicine workflows. North America dominated the market with a 41.83% share in 2025, while Asia Pacific is projected to record the fastest regional growth over the forecast horizon.

Get a Sample Research PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/116063

Key Market Drivers

Rising adoption in genomics and precision medicine is the primary market driver. Computational biology tools are essential for analyzing vast genomic, transcriptomic, and multimodal datasets and converting them into actionable clinical insights. As healthcare systems and life science organizations advance precision medicine programs, demand is growing for software and platforms that support variant interpretation, biomarker discovery, patient stratification, and therapy selection — reinforcing cloud-based bioinformatics and AI-driven analytics as foundational infrastructure. In April 2025, Illumina announced a collaboration with Tempus to accelerate clinical adoption of next-generation sequencing tests through genomic AI innovation, illustrating the sector's deepening integration of data analytics and clinical application.

The growing role of AI and machine learning in biological data analysis is a significant parallel trend. Life science entities are managing increasingly complex genomic, proteomic, and multimodal datasets that exceed the capacity of traditional tools. AI and ML are enabling researchers to rapidly identify patterns, prioritize drug targets, automate discovery workflows, and improve biomarker identification — all while integrating directly into scientific software platforms used daily in the laboratory. Benchling's October 2025 launch of its AI command center, designed to embed agents and predictive models within research workflows, reflects this accelerating integration.

Market Restraints and Challenges

Data fragmentation and poor interoperability are the primary constraints on market expansion. Computational biology depends on integrating genomic, clinical, proteomic, and other omics datasets from disparate systems into unified analytical workflows. In many organizations, these datasets reside on separate platforms, use different formats, and adhere to inconsistent metadata standards, making integration slow, costly, and technically complex. This slows analysis timelines, limits scalability, and delays the generation of clinically or commercially valuable insights, requiring end users to invest additional resources in data synchronization before analysis can begin.

A shortage of skilled bioinformatics and computational talent compounds the challenge. Effective deployment of these platforms requires professionals with cross-disciplinary expertise spanning biology, statistics, software engineering, AI, and data interpretation — a profile that remains scarce relative to growing market demand. The 2025 National Life Sciences Workforce Trends Report highlighted that the industry is confronting rapid technological change and increasing AI integration alongside significant workforce skill gaps, raising deployment costs and extending implementation timelines.

Market Opportunities

Rising adoption in clinical trials and disease modeling presents a significant near-term opportunity. Sponsors and research teams are increasingly deploying computational tools to enhance trial design, accelerate patient eligibility identification, facilitate biomarker-driven stratification, and model disease behavior earlier in development — improving target prioritization and lowering trial risk. Tempus AI's March 2025 acquisition of Deep 6 AI, whose platform accessed over 750 provider sites and more than 30 million patients, underscores the commercial scale of this opportunity for bioinformatics, AI, and translational informatics providers.

Segmentation Analysis

By component, the software/platforms segment led the market in 2025, accounting for 35.8% of end-user share at the pharmaceutical and biotechnology segment level, underpinned by the central role of bioinformatics platforms, molecular modeling tools, and omics analysis software in standard research workflows. Schrödinger reported 2025 software revenue of USD 200 million, reflecting the strong commercial traction of platform-led solutions. The services segment is expected to grow at a CAGR of 14.05% through 2034.

By deployment, the cloud-based segment held the leading position in 2025 with a projected 56.5% share in 2026, favored for its ability to handle extensive genomic datasets, eliminate significant upfront infrastructure costs, and enable AI-driven analytics at scale. The hybrid segment is forecast to grow at a CAGR of 13.22%.

By technology, bioinformatics and sequence analytics dominated in 2025 with a 38.2% share projected for 2026, anchored by its central role in sequencing data processing, variant interpretation, and multi-omics analysis across virtually all computational biology workflows. The machine learning/AI in biology segment is expected to grow at the fastest CAGR of 16.27% through 2034. By application, omics data analysis led with a 28.8% projected share in 2026, while biomarker and patient stratification is forecast to grow at the highest CAGR of 16.55%. By end user, pharmaceutical and biotechnology companies held the dominant share in 2025, projected at 35.8% in 2026, driven by sustained R&D investment and increasing use of AI and multi-omics platforms in drug development programs. CROs and CDMOs are expected to grow at a CAGR of 13.79%.

Regional Outlook

North America led the global market in 2025 at USD 2.15 billion, supported by a robust biopharma R&D base, high cloud and software adoption rates, and extensive precision medicine genomic data collections. The U.S. market alone is projected at approximately USD 2.04 billion in 2026, representing around 36.0% of global revenues. Europe is growing at a CAGR of 11.49%, propelled by cross-border genomic infrastructure, public health data collaboration, and progressive implementation of federated precision medicine programs; Germany and the U.K. are projected at USD 0.26 billion and USD 0.20 billion, respectively, in 2026. Asia Pacific is expected to record the highest regional growth rate, reaching USD 1.29 billion in 2026, driven by large-scale genomics expansion in China and Japan — projected at USD 0.39 billion and USD 0.35 billion respectively — alongside growing biotech investment and AI adoption across the region. Latin America and the Middle East and Africa are expanding more moderately, supported by rising interest in precision health, improving genomics programs, and growing public-sector investment in genomic medicine.

Connect with Our Expert for any Queries: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/116063

Competitive Landscape

The global computational biology market is moderately consolidated. Leading players include Schrödinger Inc., Illumina Inc., Danaher Corporation (Genedata AG), Thermo Fisher Scientific Inc., DNAnexus Inc. (all U.S.), QIAGEN (Germany), Seven Bridges Genomics, SOPHiA GENETICS (Switzerland), Tempus, and Recursion. Key strategic activities include cloud-native platform development, expanded AI and multi-omics capabilities, and cross-sector partnerships. Notable recent initiatives include Illumina's January 2026 launch of the Billion Cell Atlas to accelerate AI and drug discovery, and Schrödinger's January 2026 partnership with Lilly to expand antibody discovery workflows within its LiveDesign platform.