Coil Coatings Market Overview Analysis By Fortune Business Insights

Market Summary

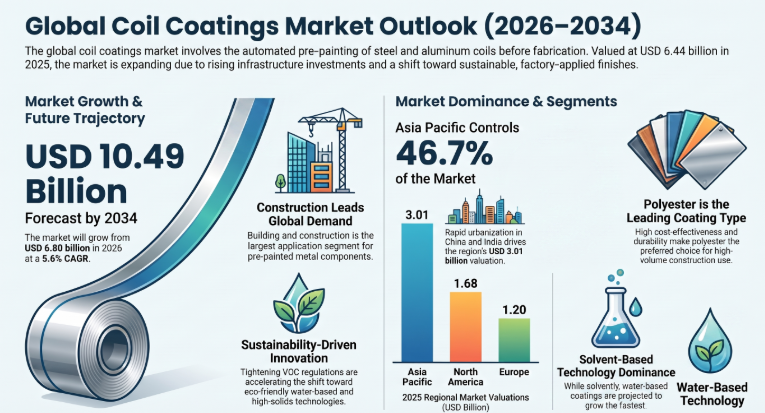

According to Fortune Business Insights: The global coil coatings market size is on a steady growth trajectory, driven by rising demand across construction, automotive, and appliance end-use industries. Coil coating is a continuous, automated industrial process in which a protective or decorative coating material is applied uniformly to rolling metal strips — most commonly steel and aluminum — before they are fabricated into finished products. The process encompasses chemical cleaning, conversion treatment, drying, primer coating, and top coating, delivering a consistent, high-quality surface finish with superior corrosion resistance and durability. The market is benefiting from the global shift toward more sustainable, high-performance surface finishing alternatives, the expansion of urban construction activity, and growing automotive production volumes worldwide. Asia Pacific is expected to emerge as the fastest-growing regional market over the forecast period, while North America and Europe maintain substantial shares anchored by mature manufacturing bases.

Get a Sample Research PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/108289

Key Market Drivers

The primary driver of coil coatings demand is the continued expansion of building and construction activity worldwide. Coil-coated metal is widely used in roofing panels, wall cladding, ceiling grids, steel doors, aluminum façade panels, and other architectural applications where durability, weathering resistance, and aesthetic consistency are essential. Rapid urbanization and infrastructure investment — particularly across emerging economies in Asia Pacific, the Middle East, and Latin America — are expanding the base of construction projects requiring pre-coated metal products. India's capital expenditure allocation of USD 133 billion in FY2024–25 and U.S. total construction spending of USD 2.2 trillion in 2024 collectively illustrate the structural strength of this demand driver.

Automotive sector growth represents a parallel and increasingly significant driver. Coil-coated steel and aluminum are used in exterior body panels, doors, underbody components, and interior structural parts, where coatings must deliver corrosion resistance, paint adhesion, formability, and noise reduction simultaneously. The ongoing growth of global passenger car production — and the accelerating transition to electric vehicles, which require lightweight, corrosion-resistant panel materials — is reinforcing demand for high-performance coil coatings, particularly in Asia Pacific, Europe, and North America. Appliance manufacturers are also consistent consumers, relying on coil-coated metal for refrigerator panels, washing machine housings, dishwasher carcasses, and HVAC components, where resistance to moisture, cleaning agents, and temperature variation is critical.

The growing preference for environmentally sustainable coatings is a third significant driver. As regulatory frameworks such as the European Green Deal tighten VOC emission limits and carbon reduction targets, producers are investing in low-VOC, waterborne, and UV/EB-curable coil coating systems that reduce energy consumption and emissions during curing. These next-generation formulations also offer competitive performance advantages over conventional solvent-borne systems, accelerating substitution in regulated markets. Technological innovation across resin chemistry and application equipment continues to improve coating efficiency, reduce waste, and enable product customization in color, gloss, and surface texture.

Market Restraints and Challenges

The most prominent constraint on market growth is the volatility of raw material costs. Coil coatings are formulated from resins, pigments, solvents, and specialty additives — all of which are petrochemical derivatives subject to significant price fluctuation tied to crude oil cycles, supply chain disruptions, and feedstock availability. These input cost swings compress producer margins and complicate contract pricing, particularly in competitive, price-sensitive construction and appliance supply chains where the ability to pass through cost increases is limited. Stringent and evolving environmental regulations covering VOC emissions, heavy metal content in pigments, and hazardous chemical use add compliance cost burdens and require ongoing reformulation investment, particularly for smaller regional manufacturers.

Segmentation Analysis

By resin type, polyester holds the dominant position in the market, accounting for the largest share across building and construction as well as consumer goods applications. Polyester coatings are widely adopted for their excellent corrosion and weather resistance, UV stability, flexibility, color retention, and cost-effectiveness across a wide range of service conditions. They are the standard choice for roofing, wall cladding, and general-purpose architectural metalwork. Polyvinylidene Difluoride (PVDF) coatings represent the fastest-growing resin segment, driven by their superior resistance to harsh weather, UV radiation, chemicals, and extreme temperatures. PVDF is increasingly specified for high-end architectural exteriors, premium building façades, and automotive and EV body panel applications where long-term durability and environmental compliance are prioritized. Polyurethane (PU) and plastisol grades serve niche performance applications requiring flexibility, impact resistance, or high film thickness, particularly in roofing and industrial applications.

By end-use industry, building and construction leads the market with the largest revenue share globally. The sector generates consistent demand for coil-coated products across roofing, wall panels, ceilings, doors, windows, and structural components in both residential and commercial construction. The automotive segment is recognized as a high-growth application, with rising vehicle production and EV platform expansion stimulating demand for lightweight coated panels. The appliances segment drives steady baseline demand for coil-coated steel in white goods and HVAC equipment, supported by rising consumer spending in emerging markets.

Regional Outlook

Asia Pacific is the largest and fastest-growing regional market, driven by China's and India's roles as the world's dominant construction markets, the region's leading position in automotive OEM production, and the accelerating pace of urban and industrial infrastructure development across Southeast Asia. Government-backed housing programs, smart city investments, and large-scale public works are generating structural tailwinds for coil-coated metal demand across the region. North America holds a substantial market share, supported by high automotive production rates in the U.S. and Mexico, strong consumer appliance demand, rising residential renovation activity, and the presence of major integrated coating suppliers. Europe is characterized by advanced regulatory standards, strong automotive manufacturing in Germany and other industrial economies, and leadership in sustainable and high-performance coating innovations. The Middle East and Africa market is growing at a more moderate pace, though large infrastructure megaprojects and expanding commercial real estate pipelines in the GCC are providing new demand vectors. Latin America is advancing steadily on the back of urbanization and growing residential construction.

Connect with Our Expert for any Queries: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/108289

Competitive Landscape

The global coil coatings market is moderately consolidated, with multinational specialty coatings companies competing alongside regional producers. Leading players profiled in the Fortune Business Insights report include AkzoNobel N.V. (Netherlands), BASF SE (Germany), DuPont (U.S.), Henkel AG (Germany), PPG Industries (U.S.), Axalta Coating Systems LLC (U.S.), Kansai Paint Chemical Limited (Japan), Dura Coat Products (U.S.), and The Sherwin-Williams Company (U.S.). Key competitive strategies include the acquisition of regional coating businesses to expand geographic coverage, investment in next-generation sustainable formulation platforms, and partnerships with metal substrate producers to develop integrated pre-coated material solutions. New product development targeting low-VOC, high-durability, and aesthetically differentiated formulations is central to long-term competitive positioning across all major markets.