Cement Additives Market Overview Analysis By Fortune Business Insights

Market Size & Growth Outlook

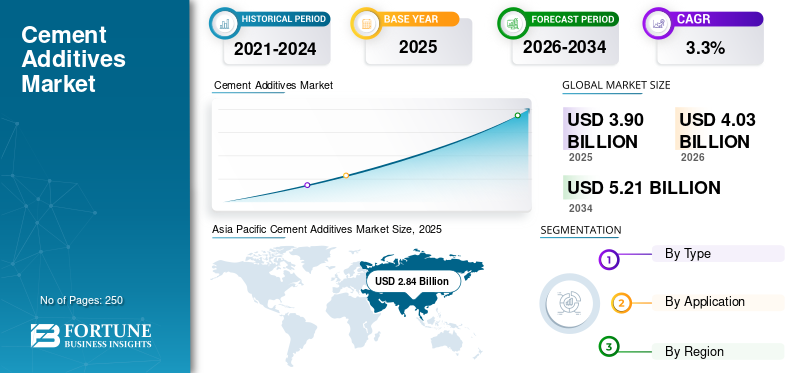

According to Fortune Business Insights: The global cement additives market was valued at USD 3.90 billion in 2025 and is projected to grow from USD 4.03 billion in 2026 to USD 5.21 billion by 2034, at a CAGR of 3.3% during the forecast period. Asia Pacific dominates the global landscape, accounting for a commanding 72.82% share in 2025, valued at USD 2.84 billion.

Cement additives are chemical and mineral-based substances incorporated during cement manufacturing or blending to improve processing efficiency, enhance cement performance, and optimize end-use properties. These include grinding aids, performance enhancers, strength improvers, and set modifiers that help boost mill productivity, reduce energy consumption, and tailor cement characteristics for diverse construction needs.

Get a Sample Research PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/116353

Market Trends

A major trend shaping the market is the growing emphasis on sustainable construction and green building practices. As the construction sector faces mounting pressure to reduce environmental impact, cement producers are turning to additives that improve energy efficiency, lower clinker factor, and enhance the performance of blended cement formulations. Regulatory frameworks such as the EU Green Deal and the Renovation Wave initiative — which targets doubling renovation rates in Europe by 2030 — are further accelerating demand for performance-oriented, sustainability-aligned cement additives.

Market Drivers

The primary growth driver is rapid urbanization and large-scale infrastructure development across both emerging and developed economies. Expanding investments in residential buildings, commercial complexes, transportation networks, and public infrastructure are increasing cement consumption volumes and compelling producers to improve grinding efficiency and cement performance. Cement additives play a vital role in helping manufacturers reduce production costs, enhance productivity, and tailor cement properties for complex construction requirements.

Market Restraints

Stringent environmental regulations on cement manufacturing emissions present a notable restraint. Cement production remains among the more carbon-intensive industrial processes, and tightening rules on CO₂ emissions, particulate matter, and energy usage are compelling manufacturers to invest heavily in cleaner technologies. This may make additive purchasing decisions more selective, particularly as producers prioritize broader capital-intensive emission-control upgrades. Additionally, regulatory scrutiny over chemical usage and formulation safety in certain regions adds complexity for additive suppliers.

Market Opportunities

The growing global shift toward green cement and low-carbon construction materials is creating significant opportunities. Cement producers are increasingly developing blended and lower-carbon formulations that reduce clinker usage while maintaining strength and durability. This transition heightens the need for advanced additives that optimize hydration behavior, improve grinding efficiency, and enhance final cement properties. As decarbonization becomes a strategic priority across the building materials sector, the role of cement additives is expected to expand substantially over the forecast period.

Segmentation Analysis

By Type: The grinding aids segment held the largest market share in 2025, driven by its critical role in improving milling efficiency, reducing agglomeration in cement mills, and lowering specific energy consumption. Their relevance is especially pronounced in Asia Pacific, where large-scale production and cost competitiveness are central to producer strategy. The performance and strength enhancers segment is projected to grow at a CAGR of 3.6% (2026–2034), supported by rising demand for high-performance cement that extends structural lifespan and enables more efficient designs. The specialty "others" category — covering set control, workability, and niche performance additives — is projected to grow at the fastest pace, at a CAGR of 4.0%, as specialized construction needs expand.

By Application: The blended cement segment led the market in 2025, driven by increasing adoption of sustainable and cost-effective cement formulations across residential, commercial, and infrastructure construction. Growing decarbonization initiatives and stricter sustainability targets are sustaining demand for additives used in blended cement production. Portland cement maintains steady demand in cost-sensitive markets and is expected to grow at a CAGR of 3.0%, supported by ongoing urbanization and housing development in emerging economies.

Regional Outlook

Asia Pacific dominates the global market with a 72.82% share (USD 2.84 billion in 2025), driven by high cement production volumes, large-scale infrastructure activity, and continued urban construction in China and India. China alone is expected to reach USD 1.88 billion in 2026, representing approximately 46.6% of global demand. India is projected at USD 0.33 billion in 2026, one of the most significant contributors to regional growth, backed by expanding residential construction pipelines and large national infrastructure programs.

Europe reached USD 0.39 billion in 2025 and is expected to grow at a CAGR of 2.8% through 2034. The region represents a technically advanced market shaped by sustainability priorities, low-clinker cement transitions, and energy-efficient grinding demands. Germany leads in the region (USD 0.08 billion in 2026), followed by the UK at USD 0.03 billion.

North America reached USD 0.23 billion in 2025, with the U.S. estimated at USD 0.21 billion in 2026. Growth is supported by building renovation activity, highway and bridge upgrades, and demand for performance-consistent cement formulations.

Latin America reached USD 0.21 billion in 2025, with Brazil — the region's largest contributor — projected at USD 0.11 billion in 2026, supported by its large construction base and housing activity.

Middle East & Africa reached USD 0.22 billion in 2025, with demand driven by infrastructure investment, urban expansion, and large-scale development projects across Gulf nations and major African markets.

Connect with Our Expert for any Queries: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/116353

Competitive Landscape

The cement additives market is led by global construction chemical manufacturers including Sika AG (Switzerland), Chryso (France), Master Builders Solutions (Germany), GCP Applied Technologies (U.S.), WACKER Chemie AG (Germany), MAPEI S.p.A., and MUHU (China). Players compete on formulation expertise, grinding efficiency support, clinker reduction capabilities, and technical services for low-carbon cement systems.

Key recent developments include Sika's acquisition of MBCC Group (May 2023), strengthening its scale in construction chemicals; MAPEI's launch of a 32,000-square-foot admixtures plant in Denver (September 2024); Master Builders Solutions' acquisition of a 51% stake in Turkey-based MBT Tech (December 2024); and the inauguration of a new MBT manufacturing plant in Navi Mumbai, India (September 2025) to support growing regional demand.