Barium Carbonate Market Overview Analysis By Fortune Business Insights

Market Summary

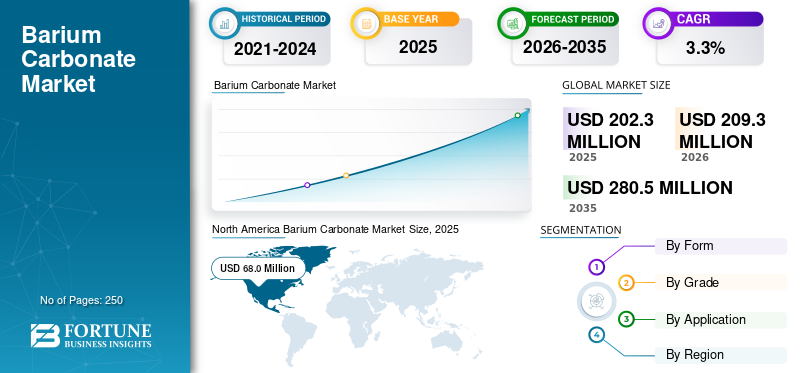

According to Fortune Business Insights: The global barium carbonate market was valued at USD 202.3 million in 2025 and is projected to grow from USD 209.3 million in 2026 to USD 280.5 million by 2035, at a compound annual growth rate (CAGR) of 3.3% during the forecast period. Barium carbonate (BaCO₃) is a white, odorless, crystalline inorganic compound used across ceramics, specialty glass, and electronics as a flux, purifier, and chemical precursor. North America held the leading regional share at 33.61% in 2025, while Asia Pacific is expected to record the most significant growth over the forecast horizon.

Get a Sample Research PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/113128

Key Market Drivers

Accelerating construction activity worldwide is the primary engine of market growth. Rapid urbanization, rising housing demand, and large-scale infrastructure investment are driving increased production of bricks, roof tiles, wall tiles, and vitrified flooring. Barium carbonate is added to clay mixes to neutralize soluble sulfates, converting them into stable barium sulfate, thereby preventing white salt stains, scumming, and efflorescence while improving the durability and fired color of finished products. Growing output of ceramic sanitaryware and advanced ceramics further underpins demand from this segment.

Alongside construction-linked demand, expanding electronics and specialty glass manufacturing is reinforcing market growth. High-purity BaCO₃ serves as the main barium source for barium titanate and ferrites — essential materials in multilayer ceramic capacitors (MLCCs), PTC thermistors, sensors, actuators, and magnetic components. As consumer electronics, automotive systems, and telecom hardware expand, MLCC and ferrite volumes rise in parallel, directly lifting BaCO₃ consumption, particularly for technical and electronic grades.

Market Restraints and Challenges

The market faces meaningful headwinds tied to the compound's toxicity profile. Barium carbonate is classified as harmful if swallowed or inhaled, as soluble barium ions can affect muscles and the nervous system. This has prompted stricter environmental and worker-safety regulations covering dust control, labeling, storage, and disposal, raising compliance costs for producers and downstream users. In some markets, tightening regulatory standards or customer requirements are accelerating substitution toward lower-toxicity alternatives such as strontium carbonate, particularly in brick and tile applications where dosage is being minimized.

Cost and supply instability present another ongoing challenge. Barium carbonate production depends on mined barite processed through energy-intensive high-temperature conversion. Barite prices track oil-and-gas drilling cycles and can spike when major mines are disrupted, while coal, gas, and power tariff swings compress margins further. Trade protectionism adds a further layer of uncertainty, with anti-dumping duties on imports from China and India reshaping trade flows and creating regional price disparities that affect supply chain planning.

Segmentation Analysis

By form, the powder segment dominated in 2025, driven by its uniform dispersion in ceramics and glazes and its suitability for electro-ceramic synthesis where controlled particle size is critical for dielectric performance. The granular segment is growing steadily, favored in large-scale brick, tile, and specialty glass plants for easier dosing, safer handling, and more consistent batch behavior.

By grade, the technical grade segment held the largest share in 2025, reflecting strong demand from specialty glass and electro-ceramics, where purity directly influences product performance. Tighter limits on iron, alkalis, and sulfates are now standard in electronics applications. Industrial grade remains the volume leader for construction materials, offering cost efficiency and reliable sulfate control for high-throughput operations. Niche "others" grades, including electronic-grade, laboratory, and customized low-impurity variants, command premium pricing but represent smaller volumes.

By application, bricks and tiles are expected to dominate throughout the forecast period, closely tracking global construction output. Electro-ceramic materials, including MLCCs and thermistors, represent the fastest-growing segment as miniaturization and higher capacitance requirements drive demand for ultra-fine, high-purity BaCO₃. Specialty glass, chemical compounds, and other ceramic applications round out a broadly diversified demand base.

Regional Outlook

North America leads the market through steady consumption in specialty and technical glass, advanced ceramics, and electronic-ceramic materials, supported by a mature high-value manufacturing base. Europe shows consistent demand shaped by specialty glass, technical ceramics, and regulated construction materials, with anti-dumping trade measures increasingly favoring regional suppliers. Asia Pacific is the most dynamic growth region, underpinned by large-scale housing and infrastructure expansion, dominant MLCC and electronic-ceramics manufacturing in China, Japan, and South Korea, and proximity to major barite feedstock sources. Latin America is growing gradually on the back of rising residential construction and ceramics output, while the Middle East and Africa are benefiting from infrastructure megaprojects, new ceramic tile plants, and expanding glass manufacturing.

Connect with Our Expert for any Queries: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/115006

Competitive Landscape

The market is shaped by a mix of global chemical companies and regional specialists. Key players include Solvay (Belgium), Sakai Chemical Industry and Nippon Chemical Industrial (Japan), Hubei Jingshan Chutian Barium Salt Corporation (China), Thermo Fisher Scientific and American Elements (U.S.), FUJIFILM Wako Pure Chemical Corporation (Japan), Kandelium (Germany), and Vishnu Chemicals and Akshya Chemicals (India). Companies are channeling investment into advanced refining, tighter particle-size control, and cleaner production routes to address evolving purity requirements in electronics and glass, while also working to differentiate on supply reliability and regulatory compliance.