Autonomous Data Platform Market Overview Analysis By Fortune Business Insights

Market Summary

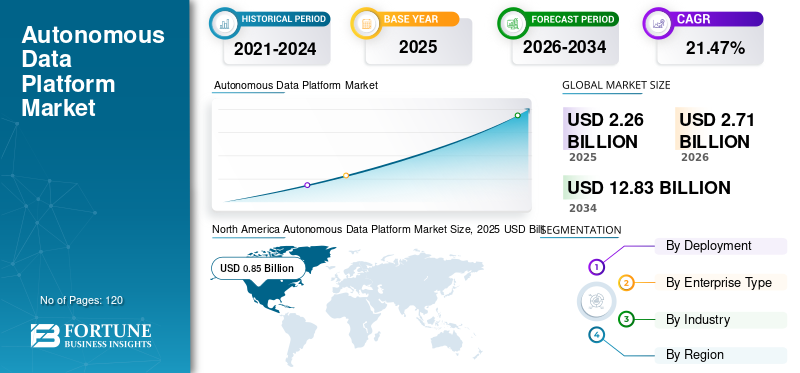

According to Fortune Business Insights: The global autonomous data platform market size was valued at USD 1.91 billion in 2024 and is projected to grow from USD 2.26 billion in 2025 to USD 9.51 billion by 2032, at a CAGR of 22.79% during the forecast period. An autonomous data platform is a self-managing big data infrastructure that monitors usage patterns, optimizes workloads, and handles tasks such as provisioning, tuning, patching, and security without requiring human intervention. It supports analytic workloads including data marts, data lakes, and business intelligence functions, enabling organizations of all sizes to extract actionable insights from large and complex datasets cost-effectively. North America held the dominant regional position with a 38.22% market share in 2024.

Get a Sample Research PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/107181

Key Market Drivers

Accelerating enterprise digitization is the primary force propelling market growth. Rapid expansion in internet penetration, mobile device adoption, and connected infrastructure is generating unprecedented volumes of structured and unstructured data, creating strong demand for platforms capable of managing and analyzing it autonomously. Organizations across BFSI, healthcare, retail, and telecommunications are increasingly modernizing their data architectures to improve productivity, reduce latency, and support real-time decision-making — all areas where autonomous platforms deliver measurable advantage over traditional database solutions.

The integration of artificial intelligence and cognitive computing is further reshaping the market. Cloud hyperscalers have embedded autonomous optimization, self-scaling, and self-healing capabilities directly into their baseline infrastructure offerings. Oracle's autonomous database revenue grew 104% year-over-year in fiscal 2025 as enterprises shifted away from manual tuning, while Amazon earmarked USD 100 billion for AWS AI infrastructure in 2025 — a clear signal that autonomy has become a foundational expectation in large-scale data operations. Snowflake's partnership with NVIDIA, enabling inference capabilities directly within the data platform, further narrows the gap between storage and AI model execution.

The COVID-19 pandemic provided additional structural momentum by accelerating cloud adoption and demand for remote data access, pushing organizations to migrate client services to virtual environments and expand investment in real-time tracking and analytics. These shifts have had a lasting effect on enterprise buying behavior, normalizing cloud-first and hybrid data architectures.

Market Restraints and Challenges

Despite strong growth momentum, the market faces several headwinds. The proliferation of complex and unstructured data creates integration challenges that can slow platform deployment. A shortage of skilled data professionals capable of configuring and managing advanced autonomous environments adds operational friction, particularly for smaller organizations. Data quality management and security concerns also remain persistent constraints, as the presence of highly sensitive organizational information heightens the need for robust governance and compliance frameworks. Stricter regional data sovereignty regulations — such as Europe's Data Act and India's data protection framework — require platforms to deliver low-latency performance while enforcing data residency controls, adding architectural complexity for global deployments.

Segmentation Analysis

By deployment, the public cloud segment led the market with a 48.40% share in 2024, driven by widespread adoption of scalable, low-maintenance infrastructure that eliminates the burden of on-premises hardware management. Cloud platforms enable access to advanced capabilities such as AI, blockchain, and large-scale analytics with reduced upfront investment. The hybrid cloud segment is projected to grow at the highest CAGR through 2032, as enterprises pursue strategies that balance public cloud scalability with private cloud security. Research indicates that enterprises using multi-cloud strategies can reduce operational costs by up to 30%, reinforcing hybrid deployment appeal.

By organization size, large enterprises held the dominant share in 2024, supported by advanced data management requirements, robust IT ecosystems, and sufficient capital to invest in enterprise-grade autonomous platforms. However, the SME segment is expanding rapidly as falling storage costs, accessible cloud pricing, and AI-driven tooling lower the barrier to adoption for smaller organizations managing growing data volumes.

By industry vertical, IT and telecommunications led the market in 2024, reflecting high adoption of data automation, governance, and compliance tools. The BFSI sector is a major consumer, deploying autonomous platforms to strengthen real-time fraud detection, risk modeling, and regulatory compliance. Healthcare and life sciences represent the fastest-growing vertical, as digitization of patient records, diagnostic data, and research pipelines creates intense demand for secure, high-performance data infrastructure.

Regional Outlook

North America commands the largest market share, anchored by a high concentration of technology leaders including Oracle, IBM, Amazon Web Services, Cloudera, and Teradata, as well as deep enterprise cloud adoption and significant public and private investment in big data infrastructure. Europe sustains steady growth driven by stringent privacy regulations including GDPR and the new Data Act, which are pushing vendors toward open-format, vendor-agnostic platform architectures with embedded lineage tracking and AI governance. Asia Pacific is expected to record the fastest regional CAGR, fueled by digital transformation programs, hybrid cloud adoption, and government-backed digital public infrastructure initiatives across India, Japan, China, and Southeast Asia.

Connect with Our Expert for any Queries: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/107181

Competitive Landscape

The market features a mix of global technology incumbents and specialized data platform providers. Key players include Oracle Corporation, IBM, Amazon Web Services, Microsoft, Cloudera, Teradata, SAP, Informatica, Snowflake, Alteryx, Denodo Technologies, Ataccama, Qubole, Gemini Data, MapR, and DvSum, among others. Companies are competing through product innovation, strategic partnerships, and capacity expansion, with autonomy, AI integration, and multi-cloud flexibility emerging as the central axes of differentiation.