Artificial Blood Vessels Market Overview Analysis By Fortune Business Insights

Market Summary

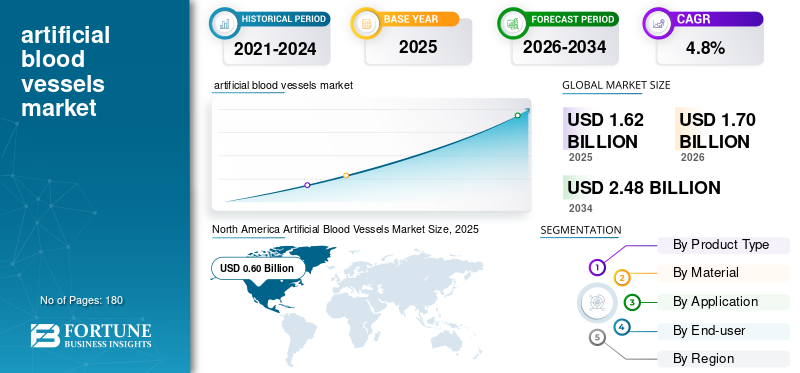

According to Fortune Business Insights: The global artificial blood vessels market was valued at USD 1.62 billion in 2025 and is projected to grow from USD 1.70 billion in 2026 to USD 2.48 billion by 2034, at a CAGR of 4.8% during the forecast period. North America led the market with a 37.03% share in 2025.

Artificial blood vessels are synthetic vascular conduits used to replace, bypass, or reconstruct damaged or diseased blood vessels when native vessels are unsuitable or unavailable. They are deployed across a broad range of clinical settings including peripheral bypass procedures, aortic repair, hemodialysis access creation, and vascular reconstruction. Growth is driven by the persistent global burden of cardiovascular disease, peripheral artery disease, kidney failure requiring hemodialysis, and an aging population that progressively demands surgical vascular intervention.

Get a Sample Research PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/109301

Key Market Trends

A defining shift in this market is the move away from treating artificial blood vessels as a broad commodity and toward using them as procedure-specific tools. Surgeons are increasingly selecting grafts based on configuration, wall thickness, surface properties, and anatomical suitability — whether for peripheral bypass, dialysis access, or aortic reconstruction. This trend is elevating the competitive value of differentiated products that offer superior handling in the operating room and more predictable long-term performance.

There is also growing overlap between open surgical and endovascular treatment pathways. Even as minimally invasive options expand, artificial grafts remain relevant in hybrid care models and for patients with more complex disease profiles. Hospitals are increasingly evaluating products on lifecycle performance — including patency rates, complication frequency, and reintervention burden — pushing manufacturers to position grafts as tools that enhance long-term care efficiency, not just implantable devices.

Market Dynamics

Drivers The primary growth driver is the steady rise in procedures linked to peripheral vascular disease, aortic aneurysm management, and hemodialysis vascular access. In peripheral artery disease, bypass surgery remains critical in limb salvage cases where endovascular treatment is insufficient. In aortic repair, prosthetic graft technologies continue to anchor open and hybrid surgical pathways. Hemodialysis access sustains recurring procedural demand, particularly arteriovenous grafts in patients who are not suitable candidates for fistula creation. Aging populations, longer survival among chronic disease patients, earlier diagnosis, and expanding specialty vascular care further reinforce market demand.

Restraints Artificial blood vessels are not always the first clinical choice. Surgeons may prefer autologous vessels for their familiarity, superior long-term patency, and lower infection risk. Clinical practice guidelines for hemodialysis still favor native fistulas where feasible, while the continued expansion of endovascular techniques reduces some cases that would otherwise progress to open bypass. Concerns about thrombosis, infection, anastomotic complications, and long-term durability — particularly in smaller-caliber applications — further narrow the addressable market. Hospital budget pressures and reimbursement scrutiny add additional constraints, especially in price-sensitive healthcare environments.

Opportunities The most significant growth opportunity lies in the development of next-generation bioengineered and tissue-engineered vascular conduits. These technologies aim to address the limitations of synthetic grafts in infection-prone or smaller-caliber applications. The bioengineered segment is projected to grow at the fastest CAGR of 9.5% through 2034. Emerging markets also offer meaningful upside as hospital capacity expands and cardiovascular and vascular surgery services become more accessible. Strategic product line breadth can further differentiate suppliers in procurement decisions.

Challenges The market's key challenge is balancing clinical complexity with commercial pressure. Graft performance varies significantly across indications, patient anatomies, and comorbidity profiles, making it difficult to standardize outcomes or market positioning. On the commercial side, hospital cost-control initiatives limit premium pricing even for technically differentiated products. The segment also sits at an inflection point between mature synthetic platforms and emerging bioengineered concepts, requiring manufacturers to sustain proven product lines while investing in longer-horizon technologies.

Segmentation Analysis

By Product Type: Peripheral vascular grafts hold the largest market share, reflecting the intersection of high disease burden and clear surgical utility in patients with severe peripheral artery disease. The hemodialysis access grafts segment is projected to grow at a CAGR of 3.9%.

By Material: ePTFE grafts dominate with an estimated 40.4% share in 2026, valued for their ease of suturing, familiar handling, and long clinical track record. The bioengineered/tissue-engineered segment is the fastest-growing material category at a projected 9.5% CAGR.

By Application: Occlusive vascular disease and bypass surgery leads all applications with a projected 30.7% share in 2026, driven by its large patient base and the continued need for surgical revascularization. Aneurysm repair is expected to grow at a 5.2% CAGR.

By End-User: Hospitals and ambulatory surgery centers (ASCs) account for approximately 76.3% of the market in 2026, as artificial vessel implantation requires full operating room infrastructure, imaging, anesthesia, and multidisciplinary teams. Specialty cardiac and vascular centers are the fastest-growing end-user segment at a 6.9% CAGR.

Regional Outlook

North America leads globally with USD 0.60 billion in 2025 (37.03% share), anchored by the U.S., which is forecast at USD 0.57 billion in 2026. The region benefits from high procedural volumes, strong hospital infrastructure, and rapid adoption of premium graft technologies.

Europe is the second-largest market, expected to reach USD 0.50 billion in 2026, driven by an aging population, established reimbursement systems, and high vascular surgical activity across Germany, the U.K., France, Italy, and Spain.

Asia Pacific is projected at USD 0.39 billion in 2026 and is expected to be the fastest-growing region. China, India, and Japan are key contributors, supported by rising chronic disease prevalence, expanding hospital infrastructure, and improved diagnostic and surgical capacity.

Latin America is forecast to reach approximately USD 0.09 billion in 2026, with Brazil and Mexico as the primary contributors. The Middle East & Africa is expected to grow steadily, led by GCC countries with stronger healthcare investment and more advanced cardiovascular centers.

Connect with Our Expert for any Queries: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/109301

Competitive Landscape

The market is moderately consolidated. W. L. Gore & Associates, Terumo Corporation, Getinge AB, and BD hold leading positions through strong surgeon relationships, broad geographic reach, and well-established graft platforms. Other notable players include LeMaitre Vascular, B. Braun SE, Artivion Inc., Braile Biomédica, Japan Lifeline, and LifeNet Health.

Key recent developments include the FDA's full approval of Humacyte's SYMVESS — an acellular tissue-engineered vessel — for extremity arterial injury in December 2024, and a Terumo Aortic and Bentley clinical study partnership announced in October 2025. These signal a broadening pipeline that blends synthetic and bioengineered approaches to meet diverse clinical needs.