Animal Feed Market Overview Analysis By Fortune Business Insights

Market Summary

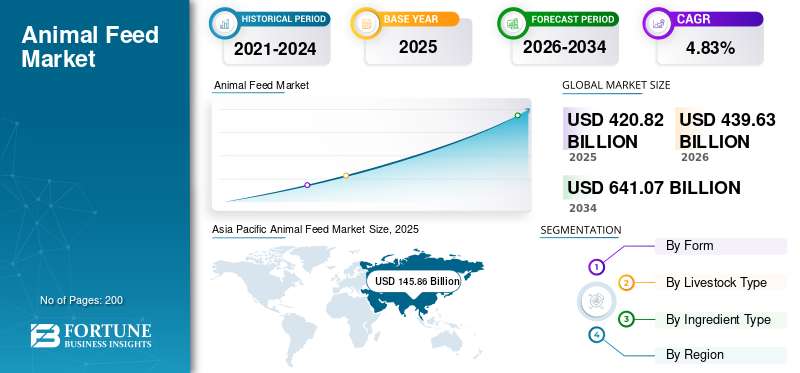

According to Fortune Business Insights: The global animal feed market size was valued at USD 420.82 billion in 2025 and is projected to grow from USD 439.63 billion in 2026 to USD 641.07 billion by 2034, at a CAGR of 4.83% during the forecast period. Animal feed encompasses specialized compound rations — typically containing grains, oilseed cakes, and essential supplements — formulated for domesticated livestock such as cattle, poultry, and fish to support optimal health, growth, and the production of meat, milk, and eggs. Asia Pacific led all regions with a 34.66% market share in 2025, reflecting its enormous livestock base and rapidly expanding protein demand.

Get a Sample Research PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/107181

Key Market Drivers

Intensifying global livestock production is the central force driving market growth. Rising populations, higher incomes, and a broad shift in dietary preferences toward animal protein are accelerating the scale of cattle, poultry, and aquaculture operations, particularly across emerging economies such as India, China, and Brazil. Livestock production in India alone accounted for approximately 31% of total agricultural gross value added in 2024, underscoring the sector's economic weight. As production systems shift from fodder-based informal feeding toward commercially formulated compound feeds rich in cereal energy and oilseed protein, per-animal feed consumption rises significantly.

Technological transformation is also reshaping the sector's growth trajectory. The adoption of Industry 4.0 tools including AI, precision feeding systems, and real-time quality sensors is enabling feed manufacturers to reduce waste, improve nutritional consistency, and lower production costs. Initiatives such as North Carolina State University's development of AI-paired low-cost sensors for feed mills and the AAFCO Virtual Assistant launch in early 2026 illustrate the increasing integration of data-driven solutions across manufacturing and regulatory functions alike.

Market Restraints and Challenges

Raw material price volatility presents the most persistent constraint on market expansion. Feed ingredients — primarily corn and soybean meal — account for more than 75% of total livestock production costs, meaning that commodity price swings pass through directly to producer margins. Corn prices for feed use rose to USD 4.58 per bushel in early 2025, reflecting the sensitivity of feed economics to agricultural market conditions. Stricter food safety regulations, such as FSMA requirements in the United States, further raise compliance and processing investment burdens, particularly for smaller producers with limited capital flexibility.

Market Opportunities

Strategic mergers and acquisitions are emerging as a key growth lever, enabling companies to localize sourcing, diversify supply chains, and reduce tariff exposure. In March 2026, De Heus Animal Nutrition's acquisition of CJ Feed & Care extended its footprint across Vietnam, Indonesia, Cambodia, South Korea, and the Philippines, exemplifying how cross-border consolidation is opening new regional markets. Expanding electro-ceramic demand for high-purity formulations and the growing feed additives segment — projected to grow at the fastest CAGR of 6.86% through 2034 — present further premium-margin opportunities.

Segmentation Analysis

By form, pellets dominated in 2025 at USD 180.88 billion, favored for their efficiency, low wastage, and compatibility with automated feeding systems across poultry and swine operations. The crumbles segment is expected to record the fastest growth at a CAGR of 5.81%, driven by preference among young animals for smaller, more digestible feed particles during starter stages.

By livestock type, poultry led the market at USD 141.16 billion in 2025. Commercial poultry systems depend entirely on compound feed across multiple short production cycles per year, generating the highest feed turnover of any livestock category. Aquaculture is the fastest-growing livestock segment with a projected CAGR of 6.32%, reflecting expanding fish and shrimp farming operations globally.

By ingredient type, cereals held the largest share at USD 206.08 billion in 2025. Corn, wheat, barley, and sorghum serve as the primary energy base across all feed formulations due to their wide availability, cost efficiency, and compatibility with protein, vitamin, and mineral blending. Feed additives including enzymes, probiotics, prebiotics, and antioxidants represent the fastest-growing ingredient category, as producers increasingly prioritize animal health, gut performance, and feed conversion optimization.

Regional Outlook

Asia Pacific remains the largest and most dynamic regional market, reaching USD 145.86 billion in 2025, anchored by China's vast pork, poultry, and aquaculture sectors and India's rapidly scaling commercial livestock base. Europe ranked second at USD 107.46 billion, driven by advanced compound feed infrastructure, strong regulatory standards, and growing demand for sustainable feed formulations and alternative proteins. North America contributed USD 92.44 billion, supported by integrated poultry and swine operations, abundant corn and soybean availability, and increasing use of precision nutrition and specialty additives. South America recorded USD 55.81 billion and is growing at a CAGR of 6.07%, underpinned by export-oriented protein industries and strong indigenous feedstock supply. The Middle East and Africa, valued at USD 19.25 billion, are advancing steadily as urbanization, rising incomes, and investment in commercial poultry and dairy systems gradually formalize feed demand across the region.

Connect with Our Expert for any Queries: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/113128

Competitive Landscape

The global animal feed market is moderately consolidated, with large multinationals competing alongside regional specialists. Leading players include Archer Daniels Midland Company, Cargill Inc., BASF SE, Chr. Hansen Holding, Kemin Industries, Nutreco (Trouw Nutrition), Charoen Pokphand Foods, Land O'Lakes Purina, Alltech, and others. Companies are directing investment toward new product development, production capacity expansion, and geographic diversification. Cargill's recent dairy feed plant opening in Punjab, India — with an annual capacity of 400,000 metric tons — and DSM-Firmenich's agreement with CVC Capital Partners to expand its Animal Nutrition and Health division reflect the scale of strategic commitment driving this market forward.