📊 Market Overview

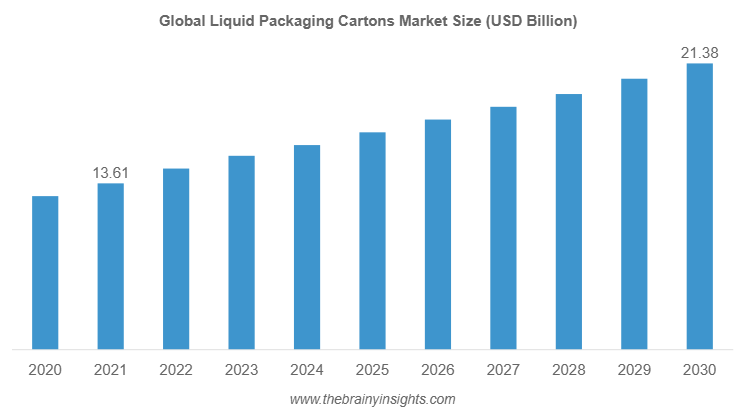

The global liquid packaging cartons market is projected to grow to USD 21.38 billion by 2030, expanding at a compound annual growth rate (CAGR) of 5.15% between 2022 and 2030.

🔄 Market Dynamics

Drivers:

- Sustainability Initiatives: Growing consumer preference for eco-friendly packaging is propelling the adoption of liquid cartons, which are often made from renewable and recyclable materials.

- Regulatory Support: Governments worldwide are implementing stringent regulations to reduce plastic waste, encouraging the use of sustainable packaging alternatives

- Convenience and Shelf Life: Aseptic liquid cartons offer extended shelf life without refrigeration, making them ideal for dairy, juice, and ready-to-drink beverages Restraints:

- Competition from Alternatives: Plastic and glass containers often offer lower production costs and greater convenience, posing challenges to the growth of the liquid packaging carton market

- Recycling Infrastructure: The effectiveness of recycling programs varies by region, potentially limiting the environmental benefits of liquid cartons

🌍 Regional Analysis

- Asia Pacific: Dominated the market with a share of 38.81% in 2024. Countries like China and India are experiencing rapid growth due to urbanization, rising disposable incomes, and increased demand for packaged beverages and dairy products

- North America: Held a significant market share of 30.1% in 2024. The U.S. market is projected to reach USD 14.3 billion by 2034, driven by health-conscious consumers and the popularity of plant-based beverages

- Europe: Accounted for 22.1% of the market share in 2024. Stringent environmental policies and consumer demand for sustainable packaging are fueling growth in countries like Germany and France

- Latin America & Middle East & Africa: These regions are witnessing moderate growth, with increasing demand for long shelf-life beverages and government initiatives promoting sustainable packaging

📦 Segmental Analysis

- By Carton Type:

- Brick Liquid Cartons: Dominated the market due to their efficient stacking and transportation advantages .

- Gable Top and Shaped Liquid Cartons: Gaining popularity for their consumer-friendly designs and branding opportunities.

- By Shelf Life:

- Long Shelf Life Cartons: Preferred for dairy and juice products requiring extended storage without refrigeration.

- Short Shelf Life Cartons: Suitable for products with a quicker consumption cycle.

- By End-Use Application:

- Dairy Products: Significant demand due to the need for extended shelf life and convenience.

- Non-Alcoholic Beverages: Including juices and flavored drinks, driving the need for innovative packaging solutions.

- Liquid Foods and Alcoholic Drinks: Emerging segments with increasing adoption of liquid cartons.

🔑 Key Trends

- Sustainable Materials: Shift towards using biodegradable and recyclable materials like PET films instead of aluminum barriers to enhance sustainability

- Smart Packaging: Integration of QR codes and NFC tags in cartons to provide consumers with product information and enhance engagement

- E-commerce Growth: Rising online shopping necessitates robust and tamper-evident packaging solutions, boosting the demand for liquid cartons

Request PDF Brochure: https://www.thebrainyinsights.com/enquiry/sample-request/12775

🏢 Key Players

- Tetra Pak International S.A.

- Elopak AS

- SIG Combibloc Group AG

- Mondi PLC

- Greatview Aseptic Packaging Co. Ltd.

- Nippon Paper Industries Co. Ltd.

- Smurfit Kappa Group plc

- Stora Enso Oyj

- Pactiv Evergreen Inc.

- Refresco Group

These companies are focusing on innovation, sustainability, and strategic partnerships to strengthen their market positions

✅ Conclusion

The liquid packaging cartons market is poised for significant growth, driven by the increasing demand for sustainable and convenient packaging solutions. Asia Pacific and North America are leading the market, with Europe also showing strong growth due to regulatory support. Key players are focusing on innovation and sustainability to capitalize on emerging trends and meet evolving consumer preferences.

For Further Information: