Aviation Gasoline Market Overview

Market Dynamics

The aviation gasoline (avgas) market is driven by a combination of factors including the growth of general aviation, rising demand for recreational flying, and increased pilot training activities worldwide. The resurgence of piston-engine aircraft in various applications has further supported avgas consumption. However, environmental concerns regarding lead content in traditional avgas and the push toward sustainable aviation fuels (SAFs) present both challenges and opportunities for the market.

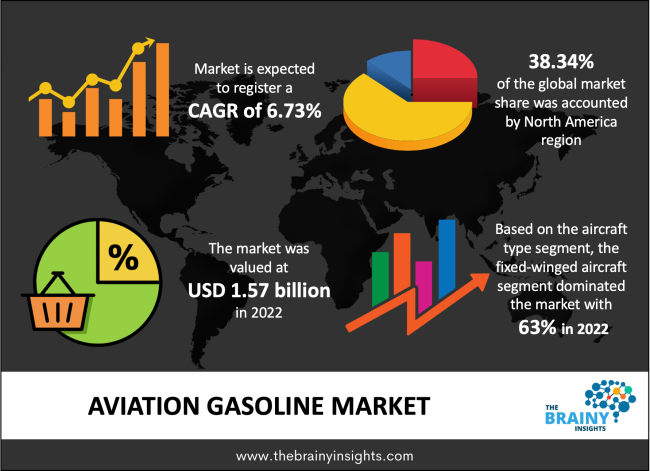

The global aviation gasoline market is projected to reach USD 2.64 billion by 2030, growing at a compound annual growth rate (CAGR) of 6.73% from 2022 to 2030.

Drivers:

- Increased global demand for general aviation aircraft

- Growing interest in private and recreational flying

- Expansion of flight training schools

- Technological innovations in piston-engine aircraft

Restraints:

- Environmental regulations and phase-out of leaded fuels

- High cost of aviation gasoline compared to alternatives

- Growing shift toward electric and hybrid propulsion systems

Opportunities:

- Development of unleaded avgas alternatives

- Market potential in emerging economies

- Investments in green aviation and sustainable fuels

Regional Analysis

North America:

Dominates the global avgas market due to the largest fleet of general aviation aircraft, strong pilot training infrastructure, and well-developed aviation services.

Europe:

Experiencing moderate growth with a strong focus on reducing emissions. Regulatory bodies are actively promoting unleaded avgas.

Asia-Pacific:

Poised for significant growth due to increasing investments in aviation infrastructure, rising disposable income, and government initiatives to improve pilot training facilities.

Latin America and Middle East & Africa:

These regions offer emerging opportunities with improving general aviation networks, although limited by infrastructure and investment compared to developed markets.

Segmental Analysis

By Fuel Type:

- Leaded Avgas (e.g., 100LL): Dominates the market but facing phase-out due to environmental concerns.

- Unleaded Avgas: Gaining traction as regulatory pressures mount and R&D efforts continue.

By Aircraft Type:

- Piston-engine Aircraft: Primary consumers of avgas.

- Light Sport Aircraft: Growing segment with increasing recreational use.

- Military Trainer Aircraft: Small but steady demand base.

By End-User:

- Private Owners

- Flight Schools

- Military

- Aero Clubs & Charter Operators

List of Key Players

- ExxonMobil Corporation

- Shell Aviation

- TotalEnergies

- Phillips 66

- BP (Air BP)

- Chevron Corporation

- Avfuel Corporation

- Swift Fuels

- Repsol

- World Fuel Services

These companies are actively engaged in R&D to develop sustainable and unleaded aviation fuel alternatives, in line with changing regulatory standards.

Key Trends

- Transition from leaded to unleaded avgas

- Technological advancements in fuel formulations

- Increased regulatory scrutiny on emissions

- Rise in electric and hybrid propulsion aircraft

- Partnerships between fuel providers and aircraft manufacturers

Request PDF Brochure: https://www.thebrainyinsights.com/enquiry/sample-request/12965

Conclusion

The aviation gasoline market is at a pivotal point, balancing traditional growth drivers with increasing regulatory and environmental challenges. While the current demand is largely sustained by general aviation and pilot training, the future hinges on innovation in cleaner, more sustainable fuel alternatives. Stakeholders who invest in green aviation and adapt to evolving fuel standards are expected to gain a competitive edge in the years to come.