Global Automotive Instrument Cluster Market to Reach USD 22.2 Billion by 2032, Fueled by Digital Transformation and EV Adoption

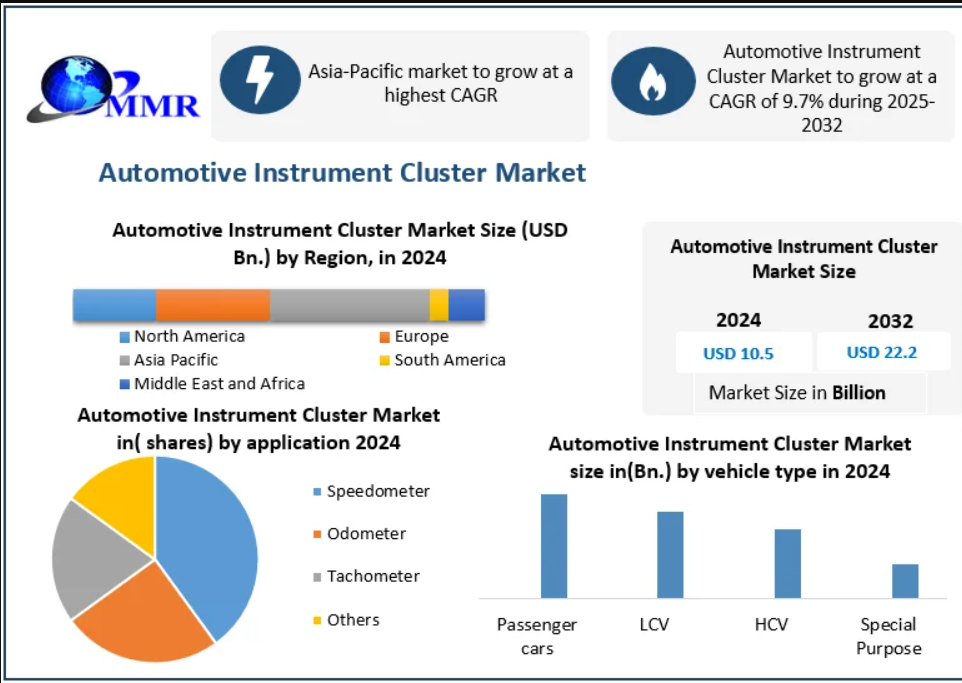

The global Automotive Instrument Cluster Market, valued at USD 10.5 billion in 2024, is projected to nearly double and reach USD 22.2 billion by 2032, expanding at a CAGR of 9.7% from 2025 to 2032. The market is undergoing a major transformation as traditional analog dashboards give way to fully digital and hybrid instrument clusters, catering to the demands of electric mobility, connected vehicles, and immersive driver experiences.

Market Overview

An automotive instrument cluster is the central display unit that provides drivers with real-time vehicle information such as speed, mileage, fuel levels, engine status, and warning indicators. Modern clusters go beyond basic functions, integrating electronic control units (ECUs), advanced sensors, and connectivity features to support ADAS (Advanced Driver Assistance Systems), navigation, and infotainment.

The shift in 2024 highlighted the rapid adoption of 2D and 3D digital clusters, particularly in luxury and passenger vehicles. Automakers like BMW, Mercedes-Benz, and Audi are pioneering advanced cockpit displays, while companies like Denso, Continental, and Visteon are reshaping cluster technology with OLED, curved panels, AI-based personalization, and augmented reality features.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/57201/

Market Dynamics

Growth Drivers

- EV and Hybrid Vehicle Expansion

The global EV transition has amplified the need for advanced clusters that can display battery performance, charging status, and energy flow. - Technological Advancements

High-resolution TFT, OLED, and micro-LED technologies are enabling fully customizable, vibrant, and slimmer designs. - Integration of ADAS and Infotainment

Safety alerts, lane departure warnings, and navigation data are increasingly displayed within clusters, ensuring convenience and safety. - Consumer Demand for Premium Experiences

Drivers now expect connected, intuitive, and immersive displays that seamlessly integrate with smartphones and infotainment systems.

Market Restraints

- High cost of advanced digital clusters remains a barrier for entry-level and budget vehicles. Automakers in lower segments continue to use hybrid or analog clusters to maintain affordability.

Opportunities

- Rising demand for connected and electric vehicles opens vast opportunities for customizable clusters, particularly in Asia-Pacific and Europe, where EV adoption is accelerating.

Market Segmentation

By Product Type

- Analog – still dominant in low-cost vehicles, but declining.

- Digital – accounted for ~30–35% of the market in 2024; fastest growing segment due to EV and connected car adoption.

- Hybrid (2D & 3D) – balances affordability and advanced display features, popular in mid-range vehicles.

By Application

- Speedometer

- Odometer

- Tachometer

- Others (Warning Indicators, Navigation, Energy Monitoring in EVs)

By Vehicle Type

- Passenger Cars – dominant segment with luxury and premium cars leading digital adoption.

- Light Commercial Vehicles (LCVs) – increasingly adopting hybrid clusters.

- Heavy Commercial Vehicles (HCVs) & Special Purpose Vehicles – focusing on safety, fleet monitoring, and ADAS integration.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/57201/

Regional Insights

Asia-Pacific (45% Market Share, 2024)

Asia-Pacific leads the market, supported by China, Japan, and India’s massive automotive production and rapid EV adoption. Cost-efficient manufacturing and a robust electronics supply chain make APAC the global hub for cluster production. Automakers like Toyota, Hyundai, and Maruti Suzuki are equipping vehicles with hybrid clusters, combining affordability and advanced features.

Europe (25% Market Share, 2024)

Europe ranks second, driven by premium automakers like BMW, Audi, and Mercedes-Benz who are at the forefront of digital and AR-based clusters. Strong EV adoption, stringent emission norms, and demand for advanced safety systems fuel growth.

North America

North America is witnessing steady adoption, particularly in connected vehicles. OTA (over-the-air) updates for clusters and the integration of AI and AR-based displays are becoming increasingly standard.

Middle East & Africa / South America

These regions are in the early adoption phase, with growth led by luxury imports and gradual electrification trends.

Competitive Landscape

The market is highly competitive, with global and regional players investing in R&D to enhance display technology, AI integration, and connectivity.

- Key Players in North America & Europe: Visteon Corporation, Continental AG, Bosch, Magneti Marelli, Valeo, Aptiv.

- Key Players in Asia-Pacific: Denso Corporation, Nippon Seiki, Hyundai Mobis, Panasonic Automotive, Yazaki, Mitsubishi Electric, Pricol Limited (India).

- Emerging Tech Providers: NVIDIA, NXP, and Luxoft are contributing with software and processing solutions to enable high-performance clusters.

For example, Denso Corporation showcased a curved digital cluster at CES 2024, highlighting AI-based personalization and real-time assistance. Similarly, Continental and Audi have introduced AR clusters, blending navigation overlays with real-world visuals.

Key Market Trends

- Shift from Analog to Fully Digital: Analog displays are rapidly disappearing, replaced by TFT, OLED, and AR-enabled displays.

- Sustainability & Slim Design: Use of lightweight, recyclable components and energy-efficient displays to align with eco-friendly design.

- OTA Updates: Over-the-air software updates for clusters are becoming a norm, particularly in connected vehicles.

- AR & AI Integration: AI-personalized dashboards and augmented reality displays are revolutionizing driver engagement.

Recent Developments

- 2024 – Continental and Audi launched augmented reality instrument clusters in premium vehicles.

- 2024–2025 – OLED panoramic displays (up to 27”) gained traction, led by BMW and Hyundai Mobis.

- 2025 – Visteon and Marelli launched AI-personalized clusters, capable of learning driver habits.

- 2024 onward – OTA-enabled clusters became standard in connected cars across North America and Europe.

Conclusion

The global automotive instrument cluster market is entering a transformative decade. With the convergence of digitalization, electrification, and connectivity, clusters are no longer just functional panels but have evolved into intelligent, interactive, and safety-critical cockpit solutions.

Asia-Pacific leads the market due to its robust EV ecosystem, while Europe remains a hotspot for premium, AR-driven clusters. Companies investing in OLED, AR, AI personalization, and sustainable designs are set to dominate this fast-growing market, which will nearly double in value by 2032.