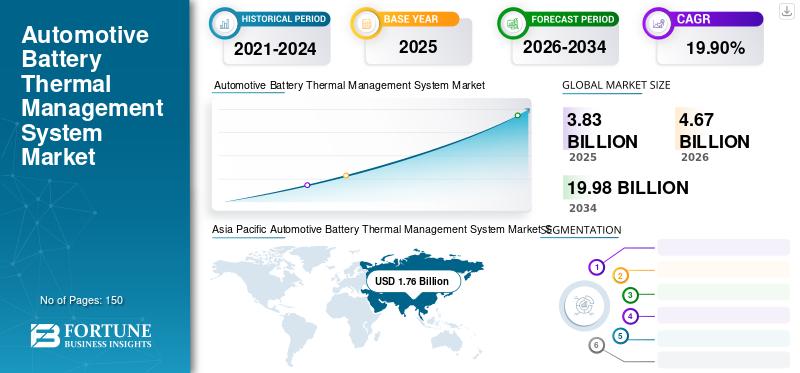

The global Automotive Battery Thermal Management System market size 2026 was valued at USD 3.83 billion in 2025 and is projected to grow from USD 4.67 billion in 2026 to USD 19.98 billion by 2034, registering a robust CAGR of 19.90% during the 2026–2034 forecast period.

Battery thermal management systems are critical electronic hardware solutions designed to prevent battery failures and maintain safe operating conditions in electric and hybrid vehicles. EV batteries function optimally within a narrow temperature range of 20°C to 40°C, making these systems indispensable for vehicle performance and safety.

Key Market Drivers

1. Surging Electric Vehicle Adoption The accelerating shift toward electric mobility globally is the primary force driving BTMS demand. Countries across Europe — including Norway, the UK, and the Netherlands — have committed to phasing out conventional internal combustion engine (ICE) vehicles. North American governments are also enforcing EV mandates. This policy-driven transition is creating sustained long-term demand for thermal battery management systems.

2. Rising Preference for Lithium-Ion Batteries Lithium-ion batteries dominate the EV landscape due to their higher energy density, longer life cycles, and superior resilience. However, their sensitivity to temperature fluctuations requires advanced thermal regulation. The growing deployment of li-ion batteries across passenger cars, commercial vehicles, and industrial machinery continues to expand the BTMS market.

3. OEM Innovation and Product Expansion Leading OEMs and suppliers are continuously developing advanced thermal management solutions. For instance, Valeo has developed smart thermal management technologies that can extend battery range by up to 30% across seasons using electrically driven compressors (EDCs) for cooling and climate control.

Get a Free Sample PDF - https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/automotive-battery-thermal-management-system-market-105522

Market Restraints

The primary challenge facing the market is the high design complexity and manufacturing cost of BTMS. Integration of these systems adds significant expense to EV production, making affordability a concern — particularly in price-sensitive markets. Challenges such as validating thermal component designs, managing coolant systems, minimizing power requirements, and reducing overall vehicle weight continue to hinder wider market penetration.

Segmentation Analysis

By Propulsion Type: The HEV (Hybrid Electric Vehicle) segment held the largest market share in 2026 due to its dual-transmission advantage in regions with limited charging infrastructure. The BEV segment is expected to grow most rapidly throughout the forecast period.

By Technology: The air cooling & heating segment currently leads the market, valued at approximately USD 1,774.1 million in 2025, owing to its simplicity and cost-effectiveness for entry-level EVs. However, liquid cooling & heating commands a 51.36% share in 2026, adopted by premium brands like BMW and Tesla for superior thermal performance in high-range vehicles. Phase Change Materials (PCMs) are gaining traction in premium segments.

By Battery Type: The conventional battery segment (lithium-ion, lead-acid, nickel-based) holds a dominant 76.62% share in 2026. The solid-state battery segment is expected to grow significantly, driven by superior safety, higher energy density, and faster charging capabilities.

By Vehicle Type: Passenger cars dominate with a 71.91% share in 2026, supported by rising disposable incomes, urbanization, and consumer preferences for advanced vehicles. Commercial vehicles show a growing but comparatively smaller contribution.

Regional Insights

- Asia Pacific leads globally with a 45.93% market share in 2025 (USD 1.76 billion), driven by China's rapid urbanization and strong government EV policies. China is projected to grow at a CAGR of 22.7%.

- Europe holds the second-largest position with a projected CAGR of 22.1%, led by Germany, supported by stringent emission standards and high EV adoption in countries like Norway and the Netherlands.

- North America ranks third, underpinned by high technology adoption and the presence of major BTMS players in the U.S. and Canada.

Key Players

Major companies profiled include Valeo (France), Hanon Systems (South Korea), Robert Bosch GmbH (Germany), Continental AG (Germany), MAHLE GmbH (Germany), GENTHERM (U.S.), LG Chem (South Korea), Samsung SDI (South Korea), Dana Limited (U.S.), and VOSS Automotive GmbH (Germany).

Recent milestones include BorgWarner's 2023 contract win for High Voltage Coolant Heaters across three EV platforms, and MAHLE's MoU with ProLogium to develop thermal solutions for next-generation solid-state batteries.

Conclusion

The Automotive Battery Thermal Management System market stands at a pivotal growth juncture, propelled by the global electrification of transportation, advancing battery technologies, and strong government policy support. Despite cost and complexity challenges, ongoing innovation by key players and expanding EV ecosystems worldwide position the market for transformative growth through 2034.