The global aircraft leasing market size 2026 was valued at USD 194.40 billion in 2025 and is projected to grow from USD 210.57 billion in 2025 to USD 377.90 billion by 2034, reflecting a robust compound annual growth rate (CAGR) of 7.60% over the forecast period.

Aircraft leasing refers to a legally documented agreement between a lessor and a lessee, wherein the lessor provides an aircraft for a defined period in exchange for periodic payments. Rather than purchasing aircraft outright, airlines increasingly opt to lease — gaining financial liquidity, fleet flexibility, and reduced maintenance burdens. At the end of the lease term, the aircraft reverts to the lessor, typically within a period not exceeding ten years.

Key Market Drivers

1. Fleet Expansion of Low-Cost Carriers (LCCs) The rapid growth of budget airlines worldwide is among the strongest catalysts for the market. LCCs prefer leasing to avoid the capital-intensive burden of ownership, enabling them to expand fleets quickly and return aircraft when no longer needed. In India — the world's fastest-growing airline market — LCCs account for approximately 60% of total air traffic, according to Boeing's India Country Market Outlook.

2. Rising Passenger Air Traffic Global air passenger volumes reached around 6.8 billion in 2022, with commercial departures running at roughly 400 per hour worldwide. This surge in demand has pushed both legacy carriers and new entrants to lease rather than buy, preserving cash flow while scaling operations efficiently.

3. Post-COVID Resilience and Sale-Leaseback Activity The leasing sector showed considerable resilience through the pandemic. In 2020, major lessors funded approximately 55% of new Airbus deliveries, with projections pointing toward 60% in coming years. Sale-and-leaseback arrangements thrived through 2021, enabling airlines to unlock capital while retaining aircraft access.

Get a Free Sample PDF - https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/aircraft-leasing-market-107476

Market Trends

Fleet Modernization and Sustainability A significant trend reshaping the industry is the push toward next-generation, fuel-efficient aircraft and green aviation initiatives. Sustainable Aviation Fuel (SAF) production reached at least 300 million liters in 2022, tripling from 100 million liters in 2021 (IATA). IATA member airlines have also committed to achieving net-zero carbon emissions by 2050.

Engine manufacturers are contributing actively — Pratt & Whitney's PurePower Geared Turbofan family, for example, is designed to reduce emissions and operating costs for lessees.

Government Policy Support Governments are enacting targeted policies to stimulate aircraft leasing. India's Finance Act 2023 amendment, effective September 2023, exempted TDS on dividends paid by International Financial Services Centre (IFSC) aircraft leasing units, directly incentivizing domestic leasing activity.

Segmentation Analysis

By Aircraft Type:

- Narrow Body dominates, driven by LCC demand and improved range capabilities of next-generation models. In February 2024, Airbus awarded an Indian manufacturer a contract for A220 aircraft doors under the "Make in India" initiative.

- Wide Body holds around 27.59% market share, favored for long-haul international routes. Monthly lease rentals for a Boeing 777-300ER run approximately USD 1.2 million — compared to a purchase price of around USD 279 million — making leasing financially attractive.

- Regional Aircraft serves short-haul and rural connectivity needs.

By Lease Type:

- Dry Lease is the most widely adopted, as lessees bear operational costs and retain full control over aircraft management — an appealing model for cost-conscious budget airlines.

- Wet Lease is used selectively during peak traffic periods when airlines need rapid capacity boosts without the burden of crew hiring and maintenance setup.

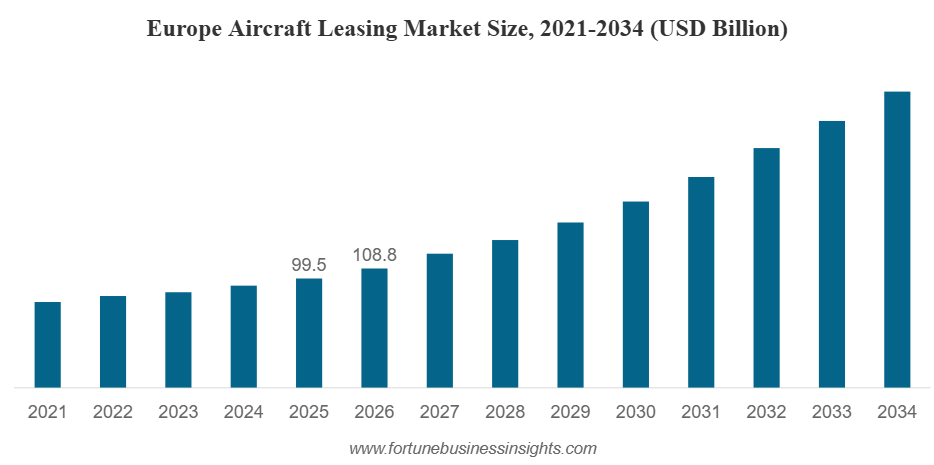

Regional Insights

- Europe leads with a 50.32% market share in 2023 (USD 87 billion), primarily due to Ireland's favorable tax environment and the dominance of AerCap, which holds over 50% of globally leased aircraft.

- North America shows moderate growth, driven by airlines shifting to leasing post-COVID; Boeing Capital Corporation remains an active player.

- Asia Pacific is the fastest-growing region, led by India and China's booming aviation sectors and rising domestic travel.

- Middle East is investing heavily in wide-body aircraft for long-haul routes, with Emirates, Qatar Airways, and DAE Capital as key participants.

Key Players

AerCap (Ireland) · Avolon (Ireland) · Air Lease Corporation (U.S.) · SMBC Aviation Capital (Ireland) · BOC Aviation (Singapore) · DAE Capital (UAE) · BBAM (U.S.) · ICBC Leasing (China) · Nordic Aviation Capital (Ireland) · Boeing Capital Corporation (U.S.)

AerCap's 2021 acquisition of GECAS gave it a combined portfolio of over 2,000 aircraft and approximately 450 next-generation aircraft on order — cementing its position as the market's dominant force.

Restraining Factor

The primary market constraint is inadequate airport infrastructure, particularly in developing economies. Aircraft lessors require well-equipped airports for storage, maintenance, and operations. The absence of modern facilities in many regions limits geographic diversification and concentrates market power in Europe and North America.